A Claude Skill Is Not an Investment Process

Claude Skills are useful, but most investors are using them wrong. They are downloading someone else’s process, then wondering why the output feels impressive but does not build conviction.

For the past couple of months, I have been writing about Claude Code for investment research, and the reaction split almost perfectly in two.

The people who actually tried it became serious fans. They got past the black terminal and realised the funny part: you do not need to be a developer to use it. You can talk to it in plain English, point it at your annual reports, your transcripts, your messy folder of consultancy PDFs, and it starts working like a research analyst sitting inside your laptop.

Most people never crossed that first barrier. They saw the terminal and quietly checked out, and I understand exactly why. Finance professionals did not spend years learning valuation, earnings power and management behaviour just to feel stupid in front of a blinking cursor. Humanity has invented many forms of unnecessary pain, and command-line anxiety is apparently one of them.

So today I want to step one layer simpler. Not away from Claude Code, because I still believe the CLI tools are where serious AI research eventually goes. But before most investors get there, they need something easier to hold.

That brings us to Claude Skills.

I started building Skills very early, right after Anthropic shipped them, and for three or four months I was obsessed. I built finance skills, broke them, rebuilt them, debugged prompts for hours, and tried to turn every repeatable piece of my research into a reusable system. It felt like real progress. The outputs looked the part, clean and structured, the kind of thing you screenshot and post.

And then something happened that I did not notice for weeks. I stopped opening them.

Nothing broke. The equity research skill still ran, the 13F screen still produced a tidy output, I just drifted away from my own work without realising it, until one day I sat with the uncomfortable question of why. The honest answer was that not one of those skills had ever changed a decision I actually made. The output was beautiful and my conviction sat exactly where it would have been without any of it. I had built a very sophisticated way of feeling like a more serious analyst.

Claude Skills are useful. But they are not the end goal.

Most people are approaching them completely wrong. They download somebody else’s investment Skill because it looks sophisticated from the outside, maybe it says Buffett-style investing or 13F framework or equity research copilot, they use it for a week, the outputs look impressive, and then they quietly stop, because the Skill never actually helped them build conviction.

Borrowing someone else’s investment Skill is like wearing someone else’s prescription glasses. For two minutes you feel sophisticated. Then you realise you cannot see properly.

That is the real problem, and it runs deeper than tooling. Investment research is deeply personal. Two successful investors can agree on eighty percent of the principles and still work completely differently, because the way they extract information, the way they connect dots, the questions they keep asking and the things they choose to ignore are never the same. You cannot inherit that from a zip file.

So this post is not a download-this-and-you-are-done tutorial. I am going to build a real investment research Skill in front of you, show you the structure, the output and the mistakes I made, but the bigger point is the one underneath it. A skill will not make you a better investor. What it can do, if you build it yourself, is force your own thinking into the open, the questions you always ask, the ones you forget, and the gaps you have been quietly walking around for years.

So here is the question I would sit with if I were you. That skill you installed last week, the equity research copilot, the Buffett framework, the 13F tracker someone handed you in a zip file. Be honest. Has it changed a single decision you have made? Or does it just make you feel like the kind of analyst who uses tools like that?

What Actually Happens After You Build Investment Skills For 90 Days

I assumed the hard part of all this would be the prompt engineering. It was not.

The hard part was how honest it forced me to be about my own research. One day I would care deeply about management commentary. The next I would lose three hours inside capital allocation. Some weeks I obsessed over industry structure, other weeks I skipped it entirely and spent all my attention on whether earnings could actually last. I had always told myself I had a process. The moment I tried to turn it into reusable instructions, I ran straight into how much of it was not a process at all.

That is what building a skill does, and it does it brutally. You see which questions you ask every single time, which ones you forget, which parts of your workflow are real signal, and which parts are just there to make you feel sophisticated while adding almost nothing to conviction.

That was the point where skills finally became useful to me. Not because they automated research, they cannot, but because building them forced me to be honest about which parts of my process were actually repeatable and worth keeping. And once I saw that, I stopped trying to build one giant equity research brain and started building small skills around the specific moments where consistency actually matters. That worked far better.

You can see this the moment two people build the same skill. Hand the same earnings-review brief to a margins-obsessed analyst and a management-quality analyst and you get two different tools. One builds it to interrogate the cost line and operating leverage. The other builds it to track what management promised last quarter against what they delivered this one. Same name on the folder, completely different instructions inside.

So before I write a single line of a SKILL.md file, before I touch folder structure or decide whether the output is a memo or a checklist, I force myself through four questions.

The Four Questions I Answer Before I Build Anything

Question One: What exact research moment is this skill meant to improve?

This sounds basic, but it is where almost every skill goes wrong. Equity research is too broad. Investment research is too broad. Even analyse a company is too broad. None of those are workflows. They are ambitions, and a skill built on an ambition will try to do everything and end up doing nothing you actually trust.

A useful skill sits inside one specific moment of your process. Reviewing an earnings call the morning after results. Comparing management commentary across four quarters. Checking whether capital allocation has quietly drifted over five years. Turning a 10-K into a list of open questions. Reading expert call notes and pulling out the things that could break the thesis. Once the moment is that narrow, the skill no longer has to pretend it can replace you. It only has to do one repeated thing well, every time.

This is also where most downloaded skills fall apart. They try to be a full analyst, because a full analyst sounds impressive in a product description. But in real research the leverage almost never comes from replacing the whole process. It comes from making one repeated step sharper and more consistent than you manage on your own.

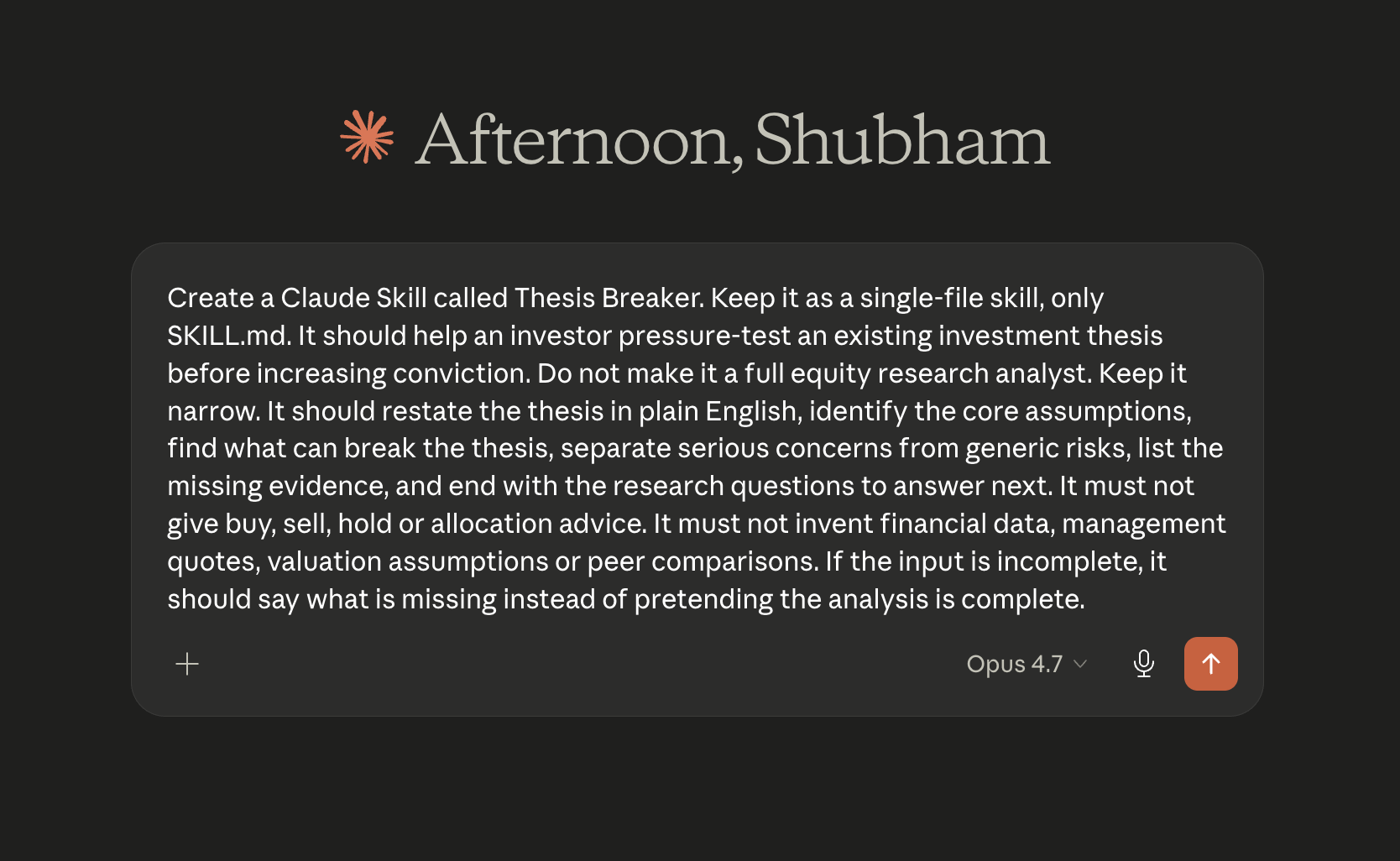

So for this post I am not going to build a complete equity research analyst. It would look impressive and it would be useless by the third run. I am going to build something deliberately narrow. A thesis-breaker.

The job of this skill is simple. You give it your thesis, along with whatever you have collected, the notes, the filings, the transcripts, and it goes looking for what could break it. It does not tell you to buy or sell. It does not pretend to know the future. It forces your own assumptions into the open and asks the questions you are most tempted to skip, the ones where the answer might cost you the position. Whether the earnings assumptions are too clean. Whether management commentary has quietly changed. Whether the valuation already prices in the good news. Whether the entire thesis is leaning on one variable behaving perfectly.

That is where AI actually helps a serious investor. Not by becoming Buffett in a zip file. By becoming a consistent sparring partner around one specific moment that matters.

Question Two: What should this skill never do?

Once the moment is clear, the next decision is not what the skill should do. It is what it should never do. This matters more in investment research than almost anywhere else, because AI gets confident far too quickly. Ask it to sound intelligent and it will. Ask it to analyse a company and it will hand you a clean, polished answer even when the evidence underneath is thin, stale or missing. A beautiful memo built on weak evidence is still weak research. It just looks more respectable while it misleads you.

So before I write the workflow, I write the boundaries. For the thesis-breaker they are simple. It does not give buy, sell or hold calls. It does not pretend missing data does not matter. It does not invent numbers, peer comparisons, management quotes or valuation assumptions. And it does not attack the thesis just to sound contrarian, because that failure is as useless as flattery. A thesis-breaker that lists every possible risk in the world looks analytical and says nothing.

A good one separates the risks that actually threaten the thesis from background noise. If the thesis depends on margin expansion, it goes after what breaks margins. If it depends on operating leverage, it tests whether revenue growth is really enough to carry the fixed cost base. If it depends on management, it compares what they said before with what they are doing now. The guardrails are not compliance decoration. They are what stops the skill from quietly turning into a confident generalist. The single rule underneath all of them: the output should make me think harder, never make the decision for me.

Question Three: What goes in?

I do not want the input to be clean, because real research never is. Sometimes you have a half-written thesis. Sometimes a page of notes from a call. Sometimes a valuation assumption sitting in your head that you have never actually written down. A useful skill has to take that messy material, work out what it has and what it is missing, and still separate the core thesis from the noise.

So the input is flexible but not lazy. At a minimum it asks for the company, the current thesis, whatever source material exists, and the specific part of the thesis you want pressure-tested. If something is missing, the skill does not paper over it. It says what it has, what it does not, and which parts of the analysis will be weaker as a result. That one choice matters more than it looks. A research skill should never reward messy thinking with a clean answer. Give it two lines of thesis and it should tell you the read is preliminary. Give it no numbers and it should not invent any.

Question Four: What comes out?

I do not want a long memo just because long memos feel serious. The output has to be short enough to read in the middle of an actual research session and sharp enough to change what I do next. For the thesis-breaker, it returns five things: my thesis in plain English, the assumptions hiding inside it, the strongest objections to it, the evidence I am still missing, and the questions I should answer before I add to the position.

That is the full design. A narrow moment, clear boundaries, realistic inputs, a useful output. Now I can stop describing the skill and actually build it.

Building the Thesis-Breaker

Now that the design is clear, I can turn it into something real. And the first decision is the one most people get wrong.

For the first version, I am keeping this deliberately simple. One folder. One SKILL.md file. That is it.

This matters because people often make Skills look more complicated than they need to be. They create multiple files, nested folders, examples, checklists, and instruction documents before the Skill has even proved that it is useful. That may look serious, but it is not always efficient.

The file tells Claude when to use the skill, what workflow to follow, what to produce, and what it must never do. If the same instructions are going to run every time, they can simply live in that one file. I would only split it later, and only if the skill earns it. If the workflow grows too large, the methodology can move into its own file. If the guardrails get detailed, they can move into another. If I start adding worked examples across sectors, those get a folder. But none of that on day one. A multi-file skill is not automatically more advanced. It is only better if the extra files genuinely reduce confusion, and on the first run they never do. They just hide the fact that you have not tested anything yet.

The goal is not the most impressive skill folder. It is the simplest version that actually works, fast enough that you can point it at a real thesis today.

Here is the prompt I would give Claude or Claude Code to build the first version.

The rest of this issue is for members. What follows is the part I can’t fake for you: the skill run live on a real Alphabet thesis, where it broke, and what it told me to build next. I opened Alpha with AI to paid members three days ago. For the next stretch, until 8 June, the first year is 25% off, my thank-you to the people who showed up before there was ever a wall.