I Taught Claude Code to Catch the Insider Buy That Never Shows Up on an Insider Feed

A director electing stock over cash leaves no trace but a footnote. I built a loop to find them, then spent the real work throwing the fakes away.

On a broking desk, insider activity arrives as a feed.

A name buys. A green row appears. A name sells. A red row appears. Somebody glances at it, says “insider buying in so-and-so,” and the row scrolls away. That was the whole ritual. The feed was the truth, and the feed only spoke in buys and sells.

I did this for months before it occurred to me to ask where the feed came from.

It comes from a filing. Every time an insider does something with their stock, they have to tell the SEC, and it’s public within two days. The feeds are just those filings, cleaned up into a table you can scan in seconds. Who, how many shares, what price. Fast and easy.

But a table can only show you what fits in a column. And there is one kind of insider decision that doesn’t fit, so the table flattens it into the most boring row on the screen.

Picture a director who is owed money. Cash. Their retainer, their fees, sometimes their actual salary. Money the company already promised them. And instead of taking it, they tell the company to pay them in stock.

Think about what that is. Not a bonus. Not shares the board handed them as a reward. A person choosing to turn guaranteed money they were owed into stock they now have to hold and hope goes up. They are giving up a sure thing for a bet. On their own company.

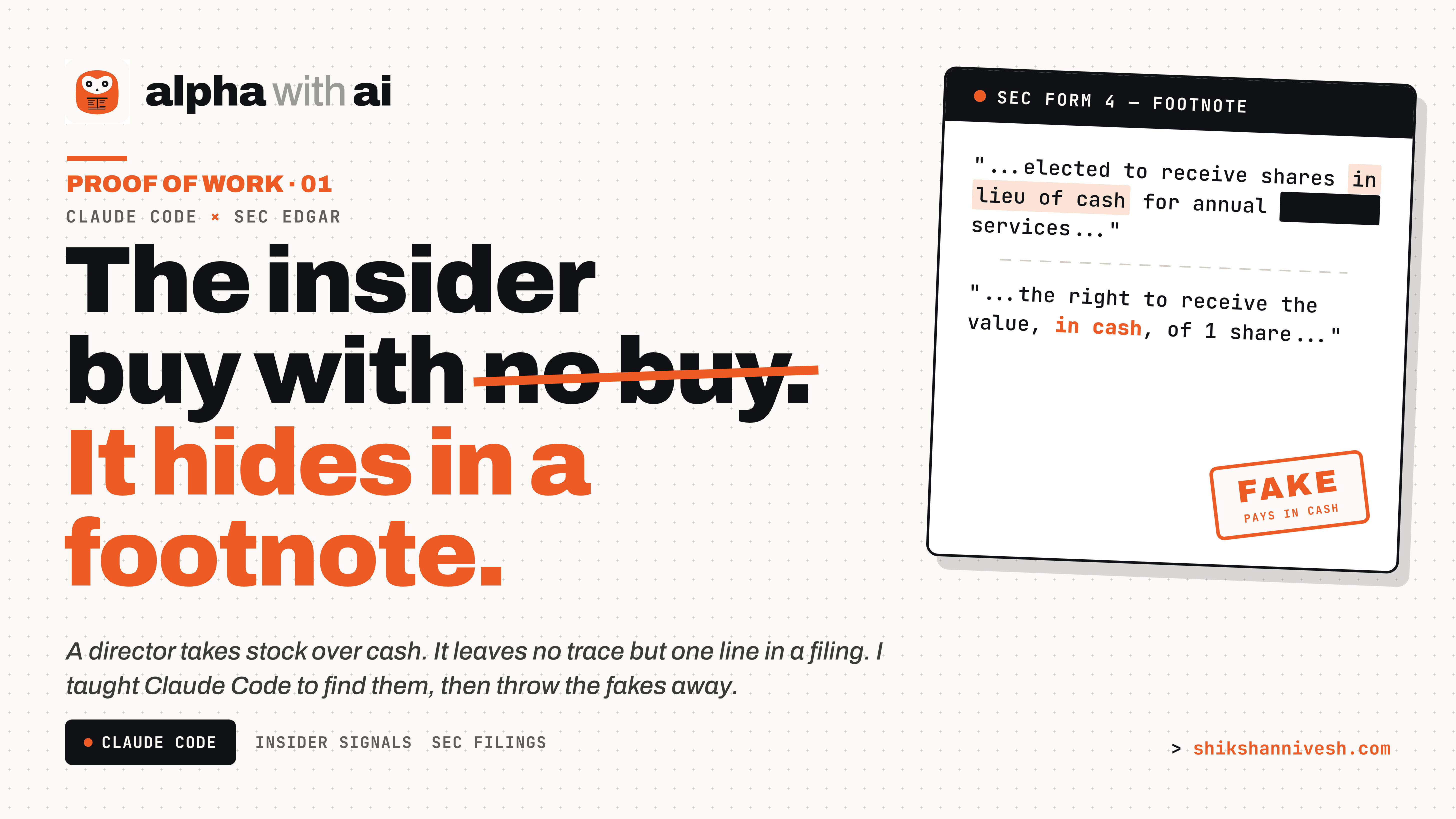

On the feed, that decision looks like nothing. It doesn’t show up as a buy, because technically they didn’t buy anything, they got paid. So it lands in the same dull pile as every routine “company gave an executive some shares” event, the kind of row everyone is trained to skip. The choice, the part that makes it interesting, the fact that they chose this, is written one line down in a footnote. And the footnote is the part the table never prints.

So the signal isn’t hidden. It’s worse. It’s sitting in plain sight, disguised as the most ignorable row on the screen, and the proof that it matters is a sentence nobody scrolls down to read.

I covered the loud version of this a while back. Open-market buys, the green rows everyone can see, the insider spending real cash. This is the quiet version. The buy that doesn’t look like a buy.

My last edition argued that the edge in this job was never the tool. It was the judgment you wrap around it. This one is me proving it. One loop, built in the open, every number traced back to the filing it came from, every wrong turn left in.

And the lesson isn’t how to find these. Finding them is easy, a minute of work, and I’ll show you. The lesson is everything that comes after, because the moment you actually read what surfaces, you learn that almost all of it is noise. And the one that looks like the cleanest signal of all might be the biggest trap in the pile.

In fact, I already have one in mind. Look at this.

Quick context before we go in. I build the AI research workflows I wish I’d had on the equity desk, then show you exactly how they run on real companies. Free to join ~5000 investors reading along. Subscribe and the next one lands in your inbox.

Why the Easy Part Is Worthless

Let me show you how easy the finding is, because it matters that you see it.

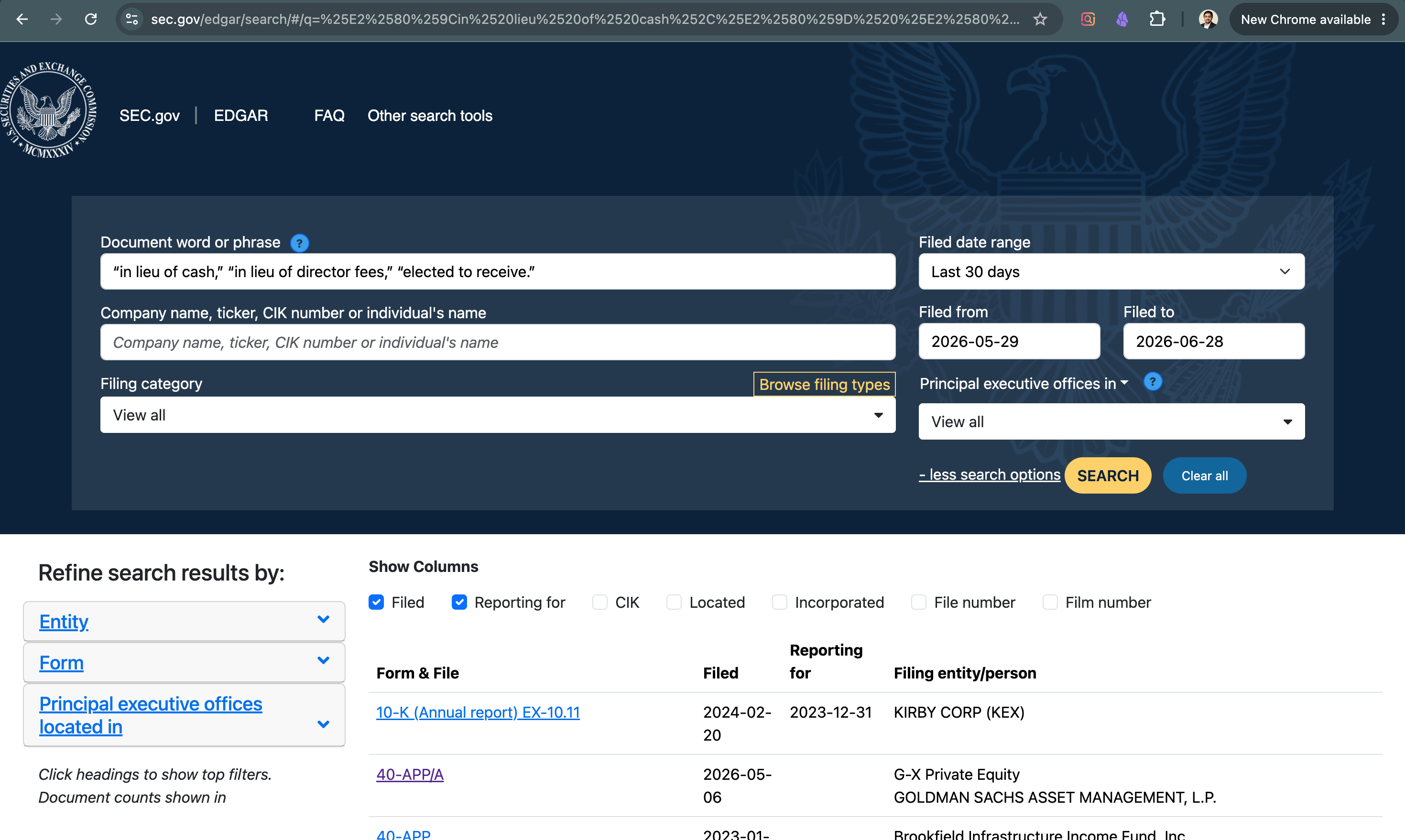

There is a search box on the SEC’s own website. It reads every filing ever submitted, including the footnotes, the part the feeds throw away. It’s free. No login, no terminal, no subscription. Anyone reading this can open it right now.

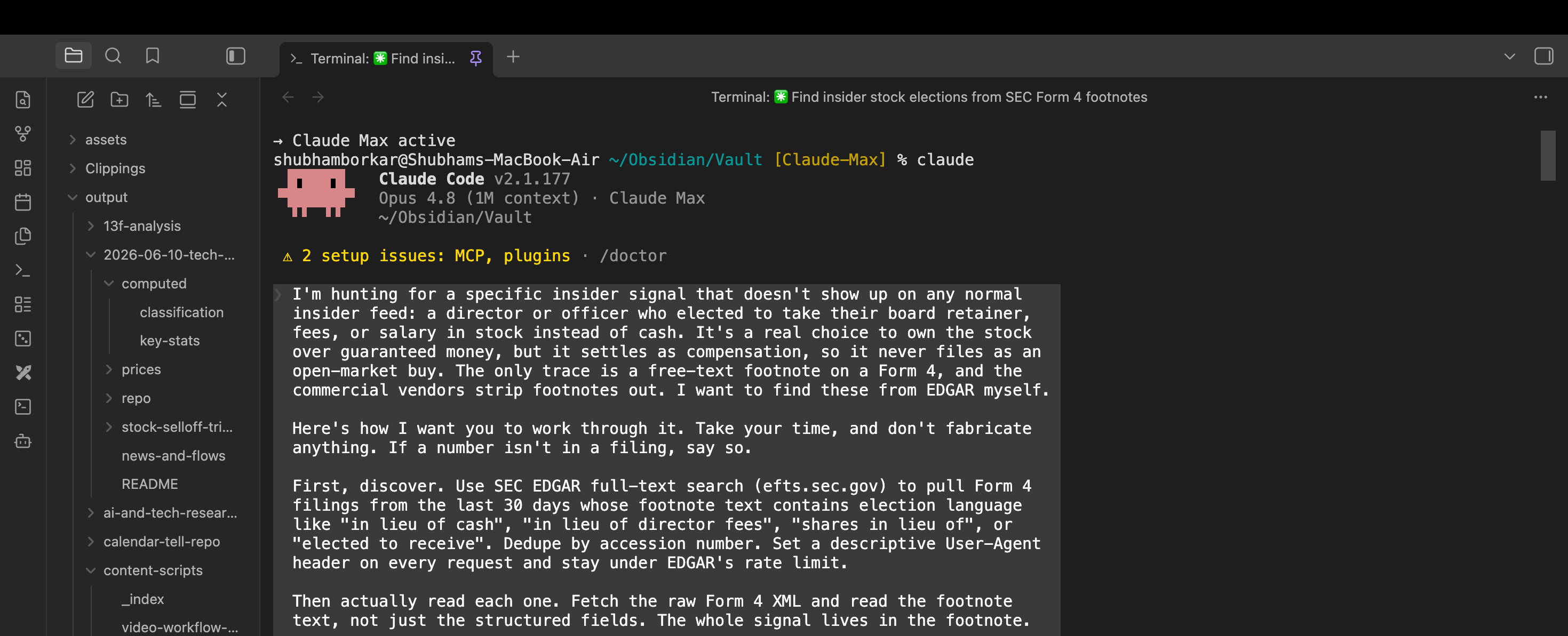

So I told Claude Code, in plain English, to go use it. Not with code. With a sentence.

Find me every insider filing in the last thirty days where someone wrote that they’re taking stock instead of cash. The phrases people actually use in these footnotes are predictable: “in lieu of cash,” “in lieu of director fees,” “elected to receive.” Search for those.

The setup that started it: How I Set Up Claude Code as My Investment Research Analyst.

It came back with a pile. Around a hundred and sixty filings once the duplicates were stripped out.

And here is the trap, the one I want you to feel before I show you the way out of it.

A hundred and sixty hits feels like a result. It feels like you found something. Your instinct, my instinct for years, is to look at that number and think the work is done. You searched, the search worked, here’s your list. Most people would stop here, post the list, and call it a signal.

That instinct is exactly wrong, and it’s the whole reason most people get nothing out of insider data even though it’s free and sitting in front of them.

Because almost none of those hundred and sixty are what you’re looking for.

The search did its job. It found every filing with the right words in it. But the right words are not the right event. A footnote can contain the phrase “in lieu of cash” and still be describing something routine, something automatic, something that isn’t a choice at all. The words match. The meaning doesn’t.

This is the part no screen and no feed will ever do for you. A search can find words. It cannot read intent. It hands you a hundred and sixty filings and it has no idea that maybe five of them mean anything. Telling those five apart from the other hundred and fifty-five is not a search problem. It’s a judgment problem. It’s the thing the machine can’t do, which means it’s the only thing you’re actually being paid for.

So the real work was never the finding. It starts now, with throwing things away.

The Three Fakes That Look Exactly Like the Real Thing

When you actually read the filings the search hands you, they sort into a few piles. Most of them are fakes. Not fakes in the sense that anyone lied. Fakes in the sense that they contain the right words while describing something that means nothing about conviction. Learning to spot them on sight is the whole skill, so let me walk you through the three that fooled me first.

The first fake is the routine grant. A company pays its directors partly in stock every single year. It’s written into the policy. Nobody chose anything. On the day the grant lands, a footnote dutifully says the shares were issued in lieu of cash, because that’s the technically correct language for how the pay is structured. The words are there. But there was no decision. The director didn’t weigh a sure thing against a bet and pick the bet. They just received their normal pay in its normal form, the same as last year and the year before. A search can’t tell the difference between a choice and a routine. You can, the moment you read it.

The second fake is the whole-board sweep. This one is sneaky because it looks like a crowd. You’ll see eight directors of the same company all “electing” stock on the exact same day. Your gut says cluster. Eight insiders, same week, same direction, that’s supposed to be the strongest signal there is. But look closer and it’s the opposite. Eight people doing the identical thing on the identical day under the identical company program is not eight opinions. It’s one corporate event wearing eight nametags. The annual meeting happened, the standing policy kicked in, everyone’s pay converted at once. There’s no individual conviction in there to find. One event, not eight. The crowd is an illusion.

The third fake is the one that nearly got me, and it’s sharp enough that it deserves its own walk-through, so I’m giving it the next section. I’ll just name it here. It’s the election that says equity and pays cash. A footnote that reads like ownership, that uses every word you’d want to see, and then, buried in the same paragraph, quietly admits the whole thing settles in money. It is a paycheck in a costume. And if you’re skimming, you will count it as a real one every time.

Here’s what survives once those three piles are swept away. A real election has a person in it. Someone who was owed cash, who could have taken the cash, and who chose stock instead, in language that shows it was their choice and not the company’s policy. Not the whole board. Not every year on schedule. A specific human being deciding to turn guaranteed money into a bet on the thing they run or oversee.

And there’s one more filter, the one that turns a real election into an interesting one. The stock has to be down.

Think about why. A director electing stock in a year the share price already doubled is electing into a party. Easy to feel good, easy to look smart, the trend is your friend. That tells you very little. But a director electing stock while the price is falling, while the chart looks ugly and the easy move would be to just take the cash and wait, that’s a different posture entirely. That’s someone reaching for more of a thing the market is actively running away from. It still isn’t proof of anything. But of all the soft signals in this pile, election into weakness is the one that’s closest to conviction, because it’s the one that costs something to make.

So that’s the target. Elective, not routine. Individual, not a board sweep. Real stock, not a cash payout in disguise. And ideally, made into a falling price.

Now let me show you that third fake up close, because it’s the one that teaches you to never trust a footnote you only skimmed.

The Filing That Says Stock and Means Cash

Here is the one that nearly slipped through, and it’s the whole reason this is a filter and not a search.

I’m not reading a hundred and sixty filings by hand. That’s the point of doing this in Claude Code. The loop pulls them, opens each raw filing, reads the footnote, and applies the test I gave it. I told it the rule up front: an election only counts if it settles in actual stock the person has to hold. If the footnote says the thing pays out in cash, throw it away, no matter how much it looks like an election.

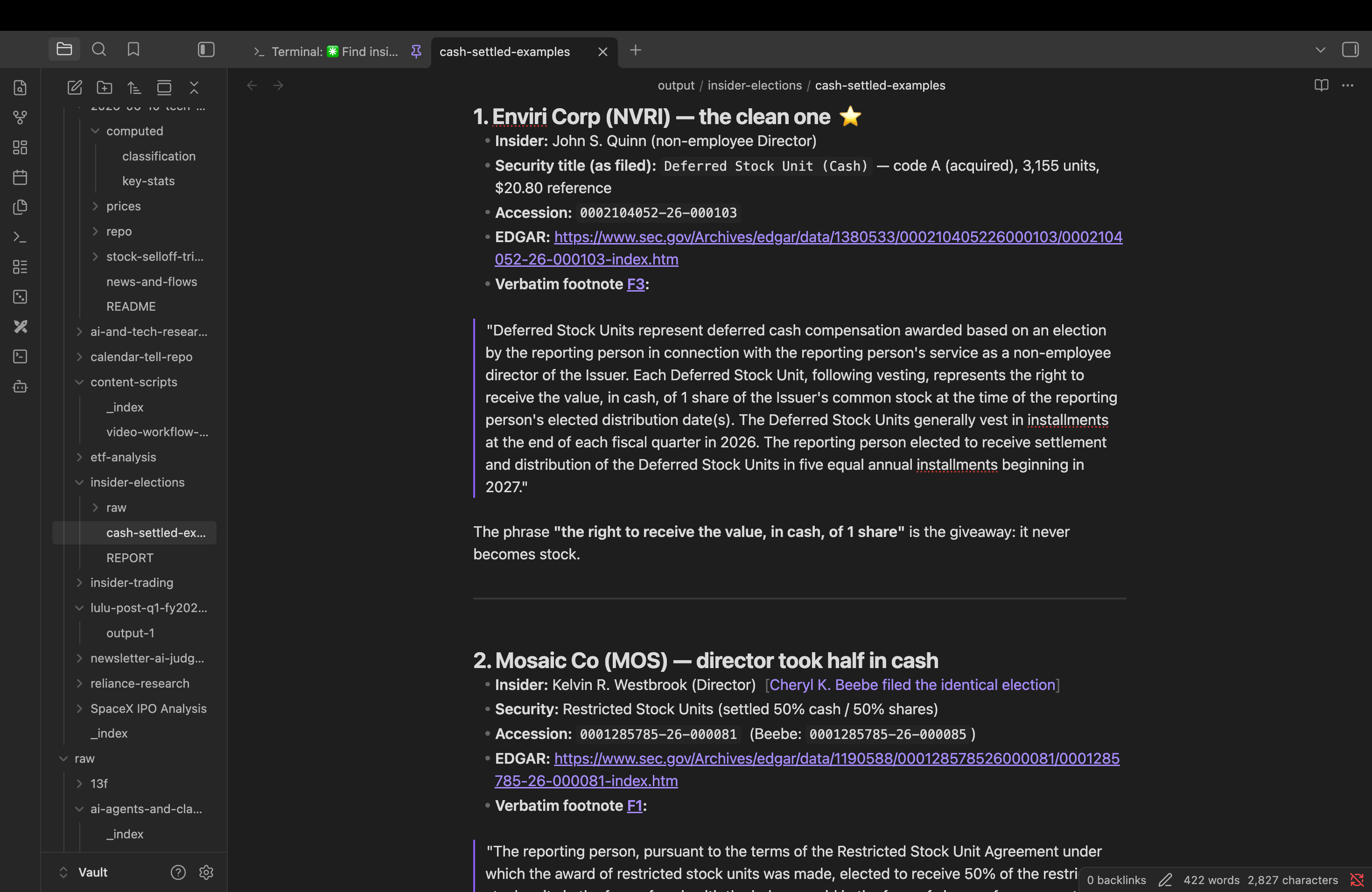

That rule is the entire reason a company called Enviri didn’t end up on my keep list.

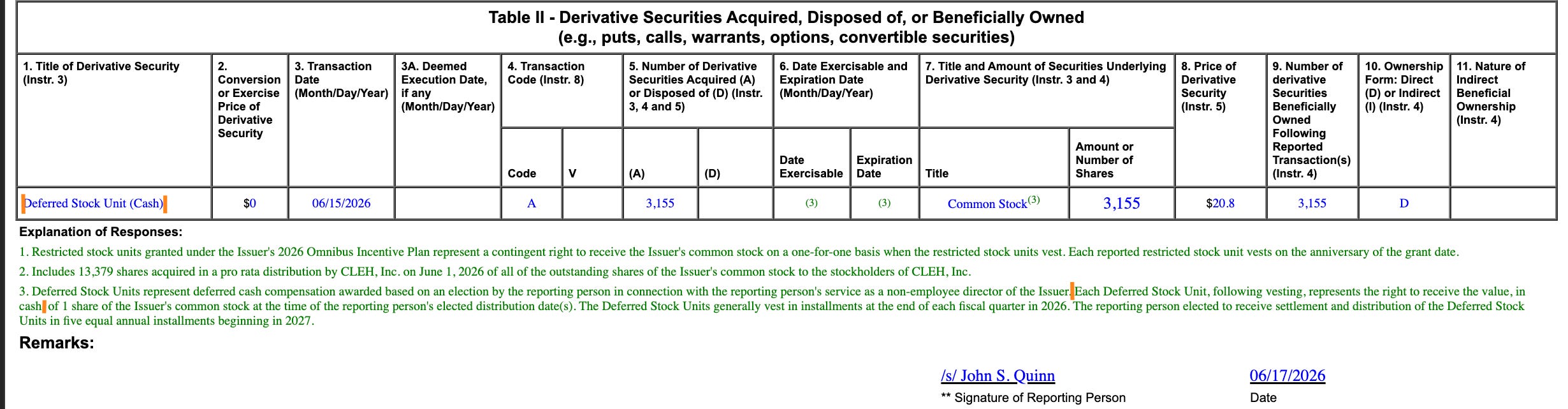

On the surface, Enviri was a perfect match. A director, John Quinn. An election he made as a director. A clean acquisition, 3,155 units, a little over sixty thousand dollars. Every word the search was looking for was in that footnote. If all you did was search for the words and trust the hits, Enviri goes straight onto your list and you tell your readers a director showed conviction. A lot of people would stop exactly there.

But the rule made the loop read to the end of the sentence, and the end of the sentence is where it falls apart.

The security wasn’t called common stock. The filing named it, in parentheses, right at the top: a “Deferred Stock Unit (Cash).” And the footnote said what that parenthesis meant. Each unit “represents the right to receive the value, in cash, of 1 share” of the company’s stock.

Read that twice, because the trap lives in one clause.

He doesn’t get the share. He gets the value of the share. In cash. Later.

So nothing here is what it looks like. It looks like a director turning his pay into stock he has to hold. What it actually is, is a director parking his pay in an account that tracks the share price and pays out in money down the road. He owns no shares. He holds a cash claim whose size happens to move with the stock. If the price doubles his eventual cash doubles, if it halves his cash halves, but he never owns a thing and he never put guaranteed money at the risk that real ownership means. He stayed in cash the whole time. The cash is just deferred and index-linked.

That is not conviction. It’s a salary deferral with a market-linked twist, closer to a bonus structure than a purchase. And it filed under the same words, matched the same search, and would have sat in the same pile as the real elections, if the only thing I’d done was search.

This is the trap, and it’s the single most common way the signal gets faked. It fools you precisely because nobody lied. Every word in the footnote is true. The director did elect. The units do track the stock. The acquisition is real. The one thing missing is ownership, and it’s missing inside a clause most eyes slide past: “in cash.”

There’s a softer version worth seeing too, also caught by the same rule. A different company, Mosaic, had directors who elected to take half their units as shares and half “in the form of cash.” Same trick, smaller dose. Half of what reads as a stock election is just cash in disguise. One director took thirty-five percent in cash instead. So if you’d seen his filing and thought “nice, a director backing the company,” you’d have been a third wrong, and nothing on the surface would have told you. Only the last line of the footnote does.

Now here’s the part I actually want you to take with you.

I didn’t catch Enviri by being a careful reader. I caught it because I knew this trap existed before I ran anything, and I told the loop to kill it. Read every footnote to the end. If it pays in cash, throw it out. The machine did that a hundred and sixty times without skimming, without getting bored, without missing the clause on filing number ninety-three at eleven at night.

That’s the whole shift, and it’s why I keep saying the finding was never the job.

The reading is done by the machine now. You don’t sit there with a hundred and sixty filings and a coffee. What the machine can’t do is know what to throw away. It doesn’t know that “in cash” quietly kills the whole signal. It doesn’t know a deferred unit is a paycheck wearing a costume. You know that. And the moment you know it, you can teach it once and let it run forever.

So the edge isn’t reading carefully. Everyone can read. The edge is knowing what you’re reading for, and that part still lives in your head, not in the tool.

Let me show you what that looks like on a name I’m keeping.

The One I Kept, and Why I Almost Believed It

After the fakes are gone, you’re left with a short list. Real elections, real people, real stock that actually gets held. And one name on my list looked better than all the rest.

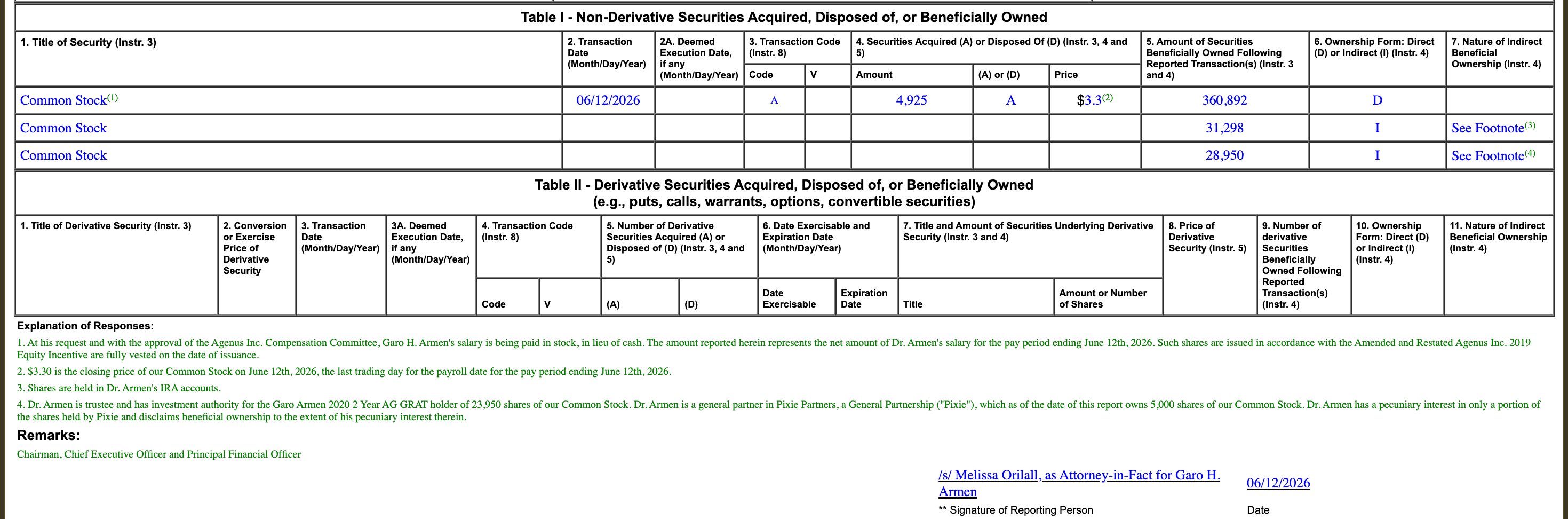

Agenus. A small biotech. The insider was Garo Armen, and he isn’t a junior board member. He’s the Chairman and the CEO. The man who runs the company.

And the footnote was the cleanest I’d seen in the whole run. Not “granted in lieu of cash,” the passive, company-driven language that makes you suspicious. This one read: “At his request and with the approval of the Compensation Committee, Garo H. Armen’s salary is being paid in stock, in lieu of cash.”

At his request.

Not the board’s policy. Not an automatic plan. His request. The chief executive asking to take his own paycheck in shares instead of money. And not once. He did it for the pay period ending in late May, then again two weeks later in June. A standing posture, repeated. The shares are fully vested the day they’re issued, so this isn’t a deferred unit that pays out later. He owns them now. Real stock, in his name, today.

And the stock is weak. It’s the chart I showed you at the start, the one I told you to hold onto. The five-dollar stock that gave it all back and kept sliding. This is the name. He’s been electing his salary into those shares the whole way down.

The rest of this one is for paid subscribers. The turn, what survived, and the claude code repo to run it yourself.