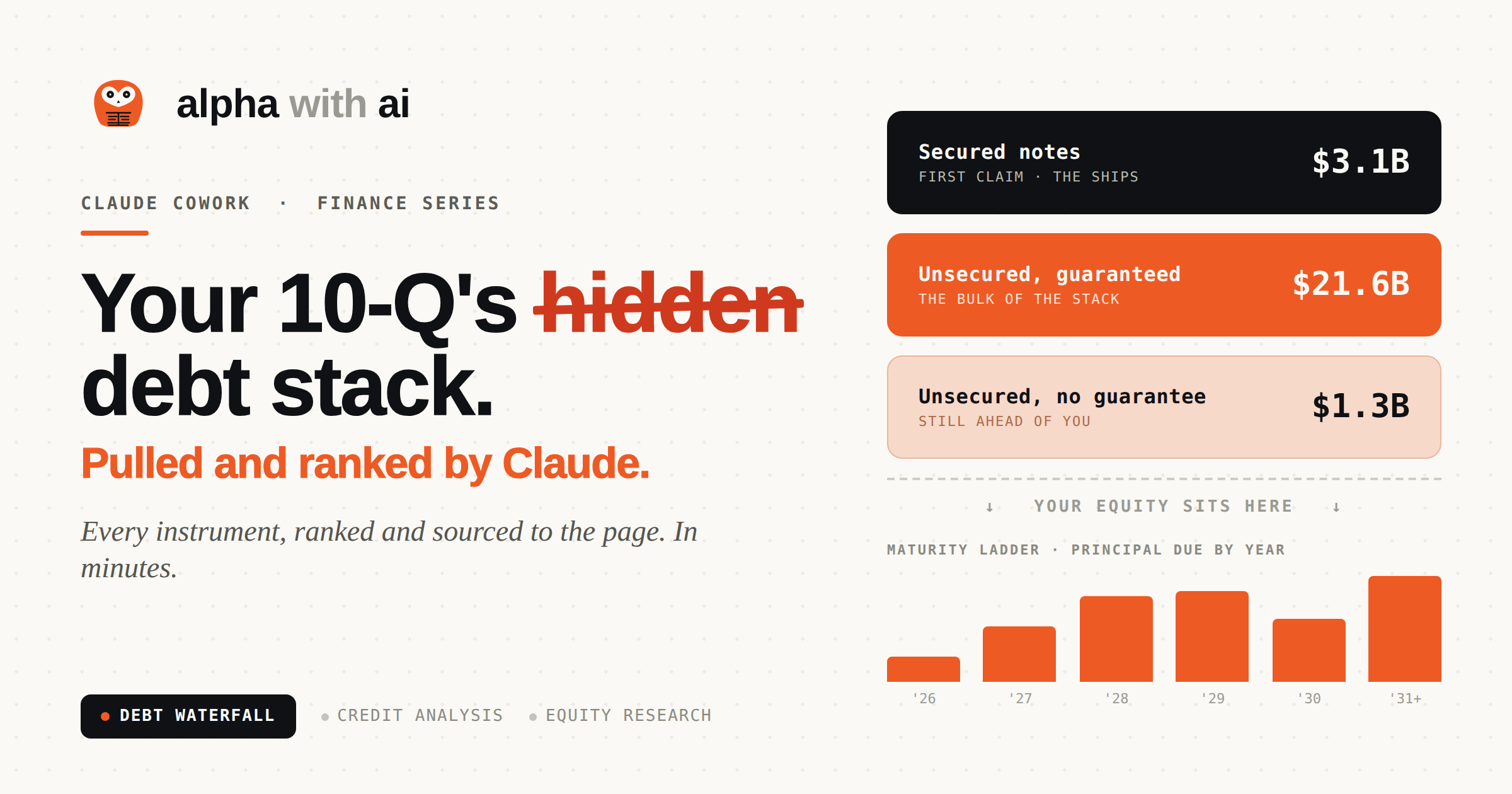

I Taught Claude to Pull a Company's Whole Debt Structure from One Filing

The most expensive thing equity and credit investors skip is the debt that gets paid before they do. I built a skill so I never skip it again.

A quick note before we start: this is one of our deepest builds yet, and it is going out free, to everyone. No paywall on this one. If you find it useful, the best thing you can do is subscribe and pass it on.

I have been in the equity market since 2018. I still make mistakes every single day.

I do not say that the way people say it when they want you to think they are humble. I say it because it is the truest thing I know about this business. I make a mistake, I sit with it, I rethink it, I learn the lesson, and then I make a slightly different mistake the next week. That is the whole job. Anyone who tells you the best investors stop making mistakes has not watched the best investors closely enough.

Look at Mohnish Pabrai and Micron. One of the sharpest value investors of his generation sold most of his Micron position in 2023, before one of the great runs in semiconductors. That is not a small investor fumbling. That is a master of the craft, and the market still handed him a regret he…