Is Big Tech's AI Capex Mispriced? I Checked, with Claude Code.

No analyst, no research desk, no data subscription. Just the filings, rebuilt in Claude Code, with every wrong turn left in.

During COVID, I screened the market every single morning.

I had no idea what I was doing.

I’d read something the night before, some ratio, some filter, some “this is what the great investors look at,” and by 9am I’d run the entire market through it. The next week I’d read something else, and the screen would change completely. The parameters I trusted back then make me wince now.

But it felt like work. It felt like being a real investor. Screen, shortlist, open the annual report of whatever came out on top, repeat. I was busy from open to close, so I told myself I was getting somewhere.

I wasn’t. Months of this, and I couldn’t point to one idea worth holding that the screen had actually handed me.

And here’s the part that took me years to admit. It wasn’t just me being a beginner.

When I started working in the markets professionally, everyone around me ran screens too. The junior analyst next to me. The PM. The most senior man on the floor, twenty years in, had his own filters he swore by. Different parameters, same ritual. Everyone was screening. Almost nobody was finding anything that way.

A couple of years back, I stopped.

Not because I found a better screen. Because I finally noticed where my good ideas were actually coming from, and it was never the screen. It was people. The investors I read. The ones I got on calls with, seasoned HNIs, operators who had been through three cycles, sometimes a junior analyst with one sharp observation. A writeup on Substack. A thread I couldn’t stop thinking about. Someone handing me not a ticker, but the question they were chasing.

That shift is the single best decision I have made as an investor. And it is exactly how I ran into the analysis I am about to show you.

I didn’t screen for it. I came across it: a video breaking down what the big four are doing with their AI spending, and it was the best take on the sector I'd seen in a long time. It stopped me cold.

Then it left me with one question.

Could I rebuild that myself? To that standard?

With Claude Code.

I know how that sounds. Most people in this business will tell you it can't be done, that serious research takes a data terminal, a team of analysts, and a budget none of us have. I'm not going to argue with them. I'm going to show you the whole thing instead, every prompt, every number, and the places I caught it getting things wrong. Don't take my word for any of it. Judge it for yourself.

This is the story of what happened when I tried.

What Claude Code Pulled First, and Why It Looks Like Madness

Here's the entire first pass in one clip, start to finish. I open the terminal inside Obsidian, paste in the prompt, and Claude Code goes out to the SEC filings on its own, pulls capex, operating cash flow and free cash flow for all four companies, and writes it all back into the vault. I handed it nothing. If you watch one thing in this piece, watch this.

If you don’t have this running yet, that is the one thing to fix before you read further, it is the biggest unlock in the whole workflow. The full setup is here: Claude code Setup

I didn’t ask Claude Code for an opinion. I already had the video’s. I gave it the idea and pointed it at the source documents instead. The 10-Ks, the 10-Qs, the earnings releases. The filings, not a summary of them.

I never left Obsidian to do it. Claude Code runs right inside the vault, in a terminal you add from the community plugins in about a minute.

My whole research library sits on the left, Claude Code works on the right, and everything it finds gets saved back into the same place. Nothing scatters across tabs and tools.

I ran this in March, when both stocks were getting hammered for the spend. I've left the prompt exactly as it was, because the question it asks is the one worth answering: is the fear justified? Reading it back now, the market has already answered for one of the two.

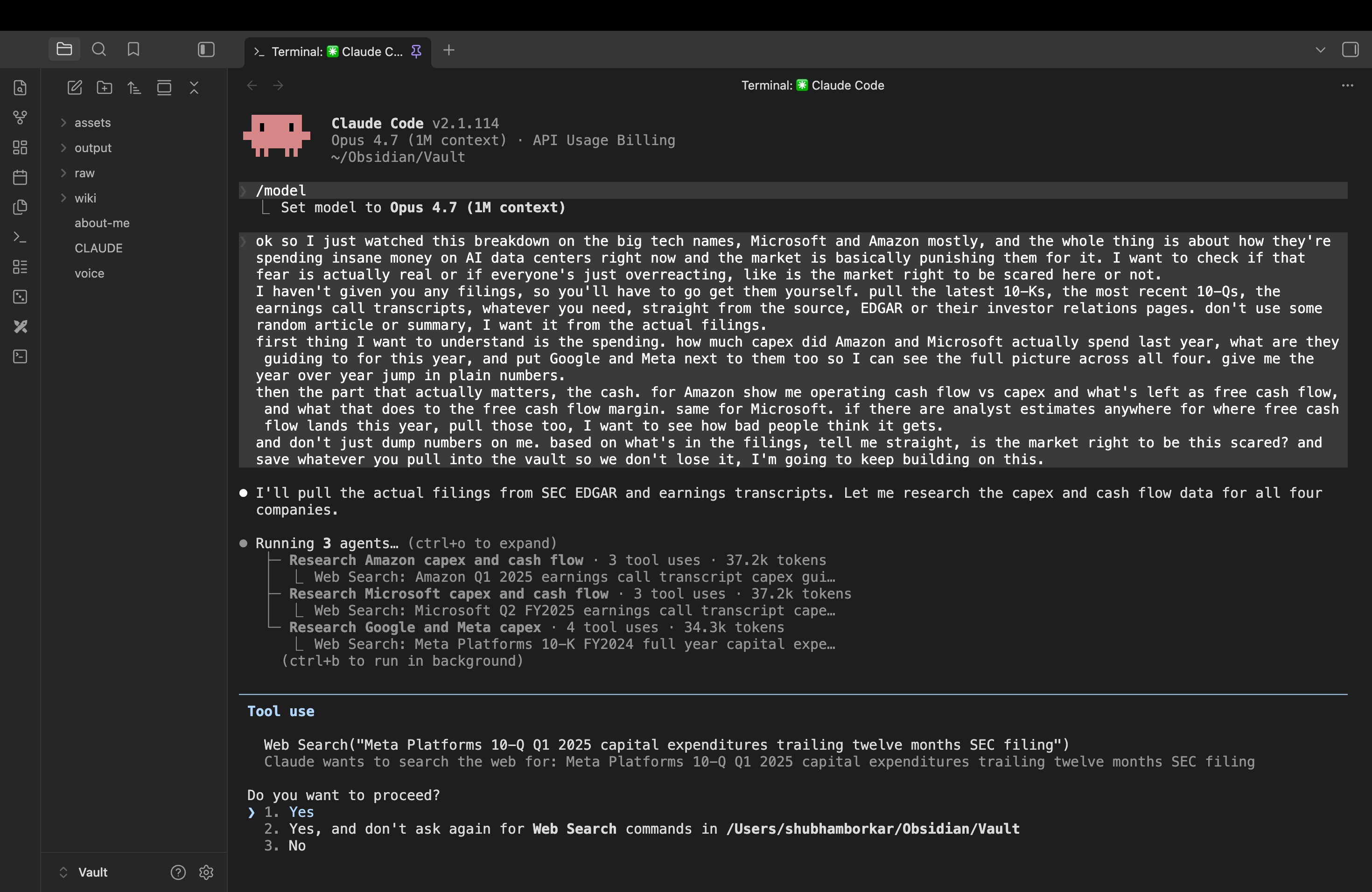

Prompt 1: ok so I just watched this breakdown on the big tech names, Microsoft and Amazon mostly, and the whole thing is about how they're spending insane money on AI data centers right now and the market is basically punishing them for it. I want to check if that fear is actually real or if everyone's just overreacting, like is the market right to be scared here or not.

I haven't given you any filings, so you'll have to go get them yourself. pull the latest 10-Ks, the most recent 10-Qs, the earnings call transcripts, whatever you need, straight from the source, EDGAR or their investor relations pages. don't use some random article or summary, I want it from the actual filings.

first thing I want to understand is the spending. how much capex did Amazon and Microsoft actually spend last year, what are they guiding to for this year, and put Google and Meta next to them too so I can see the full picture across all four. give me the year over year jump in plain numbers.

then the part that actually matters, the cash. for Amazon show me operating cash flow vs capex and what's left as free cash flow, and what that does to the free cash flow margin. same for Microsoft. if there are analyst estimates anywhere for where free cash flow lands this year, pull those too, I want to see how bad people think it gets.

and don't just dump numbers on me. based on what's in the filings, tell me straight, is the market right to be this scared? and save whatever you pull into the vault so we don't lose it, I'm going to keep building on this.The first thing it did was rebuild the spending picture from the filings. And the first number it handed back was the one that scares everyone.

Amazon spent about 77.7 billion dollars on net capex in 2024. In 2025 that jumped to 128.3 billion. A 65 percent increase in a single year. And on the latest earnings call, Jassy guided to roughly 200 billion for 2026. Microsoft ran the same play. Its capital spending went from 44.5 billion in fiscal 2024 to 64.6 billion in fiscal 2025, up 45 percent, and it has only accelerated since: the December 2025 quarter alone was roughly 37.5 billion, so even that fiscal 2025 number understates where the run rate sits today.

Then Claude Code pulled the cash, which is where it actually stings.

Amazon generated 139.5 billion in operating cash flow last year. It spent 128.3 billion of it on capex. What was left as free cash flow was 11.2 billion. The year before, that number was 38.2 billion. Free cash flow fell 71 percent in twelve months, and the share of operating cash flow Amazon got to keep dropped from 33 percent to 8 percent.

Read that cold, off the screen, and it looks like the biggest companies on earth setting fire to their own cash at the same time. That is exactly how the market read it. It is why the selloff happened.

And here is the trap. If you stopped reading the filings right here, you would sell too. Most people did.

But before I trusted a single one of those numbers, there was one step left. The one I never skip.

Rule One: I Never Trust the First Pass

The first output looked finished. Clean tables, sources listed, a confident take at the bottom. That polish is exactly when you should get suspicious.

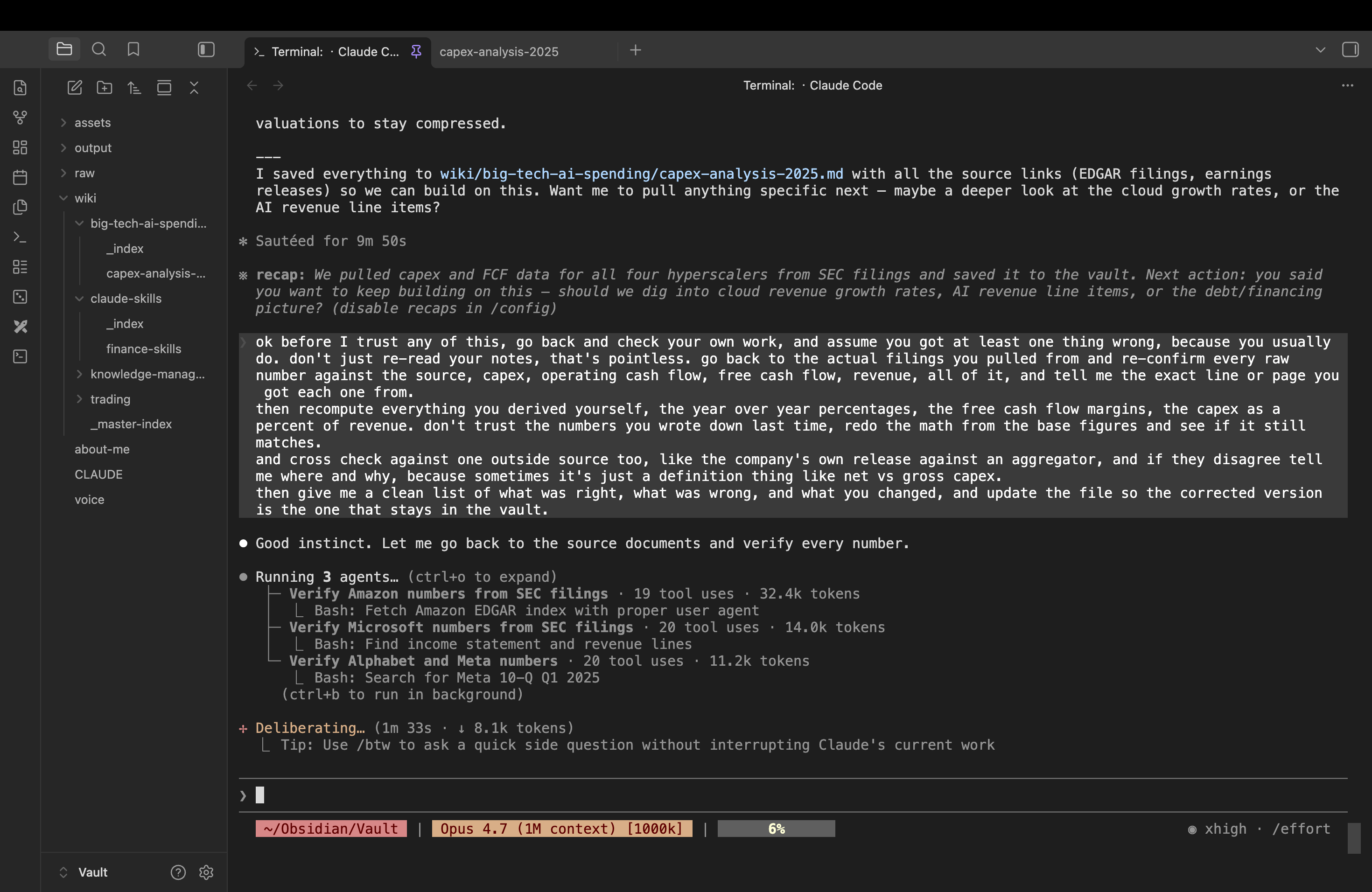

So before I believed a single number, I made Claude Code audit its own work. Not re-read its notes, that’s worthless, it just nods along with itself. I sent it back to the actual filings, line by line, told it to recompute every number it had derived, and to assume it had gotten at least one thing wrong.

Prompt 2: ok before I trust any of this, go back and check your own work, and assume you got at least one thing wrong, because you usually do. don't just re-read your notes, that's pointless. go back to the actual filings you pulled from and re-confirm every raw number against the source, capex, operating cash flow, free cash flow, revenue, all of it, and tell me the exact line or page you got each one from.

then recompute everything you derived yourself, the year over year percentages, the free cash flow margins, the capex as a percent of revenue. don't trust the numbers you wrote down last time, redo the math from the base figures and see if it still matches.

and cross check against one outside source too, like the company's own release against an aggregator, and if they disagree tell me where and why, because sometimes it's just a definition thing like net vs gross capex.

then give me a clean list of what was right, what was wrong, and what you changed, and update the file so the corrected version is the one that stays in the vault.It had. Two things, in fact. It had Microsoft’s fiscal 2025 revenue about 20 billion dollars too low, which had quietly thrown off the capex-intensity math built on top of it. And it had overstated Meta’s capex, because the first pass folded Meta’s finance-lease payments into the raw spending line.

These sound small. They are not. A wrong revenue number poisons every ratio sitting above it. And here is the one that would have actually embarrassed me: three of these four companies define free cash flow differently. Amazon nets out proceeds from asset sales. Microsoft and Alphabet don’t. Meta subtracts finance-lease payments on top of capex. Compare Meta’s free cash flow to Amazon’s without catching that, and you are quietly comparing two different things, then drawing a conclusion from a gap that doesn’t exist.

The first pass of any AI research will have errors. That is not the failure. The failure is trusting it. The discipline is the second pass, and a second pass that forces the model back to the source instead of letting it grade its own homework. That single step is the whole distance between research you can put your name on and the confident-sounding slop filling everyone’s feed.

One practical thing, because a full pass can run more than few minutes, and Claude Code pauses before most actions, so if you walk away it just sits there waiting on you. You don’t need the nuclear option to fix that, and you shouldn’t have to type yes a hundred times either.

If you just want edits to flow while you review them afterward, press Shift+Tab once for accept-edits mode. It stops asking before reading and editing inside your vault, though it still checks before risky commands or anything outside it. For a run like this one, which keeps reaching out to the web, the cleaner fix is auto mode: Claude Code runs uninterrupted while a background safety check keeps watching what it does. Either way you keep a net under you, and it still won’t touch anything outside your working folder.

There is a full bypass too, the --dangerously-skip-permissions flag, which strips every guardrail, including the one that blocks web commands. I run it on the machine that holds my research, and also I use it via my vps. If you choose to, that is your call to make. For anyone just starting out, you do not need it. Auto mode does the job.

Claude Code didn’t stop here. The next thing it pulled is what flipped the whole picture.

The Money Didn’t Burn. It Turned Into Assets.

So I went back and asked the other side of the question. If the cash is leaving, where is it going? I pointed Claude Code at the same filings, plus Amazon’s 2025 shareholder letter, to pull the part of the story the free cash flow panic leaves out.

Prompt 3: ok so the last numbers make these companies look like they're torching cash, but I don't buy that read and I want to test the other side. the whole point is capex isn't normal spending. when they buy data centers and chips they end up owning assets that earn for years, it's not gone like salaries or marketing.

first, go back into the same filings and show me the depreciation side. how much depreciation are they running now, how fast is it growing, and explain in plain terms how the capex they spend today turns into a depreciation hit over the next few years. I want to know what the real drag on reported profit actually is, because I think that's the only thing genuinely getting worse, and it's temporary next to how long these assets earn.

second, and this one matters most, pull from Amazon's own 2025 shareholder letter. Jassy talks about how the market reacted to AWS spending back around 2014 and how it played out. I want that parallel in their own words, the part about the spend and the long term and that "straight line was a lie" idea. keep any quotes short.

save it next to the capex file, and like before, don't trust your first pass, I'll verify after.Here is what the screen doesn’t show you. When a company pays salaries or runs ads, the money is gone the moment it’s spent. When Amazon spends 128 billion dollars on data centers and chips, it does not vanish. It becomes 128 billion dollars of assets sitting on the balance sheet, earning for years.

The reason it looks like a wound is timing. Capex hits the cash flow statement all at once, today. But it reaches earnings slowly, spread out as depreciation over the life of the asset, four to six years for servers, far longer for the buildings. So the cash looks terrible now, while the earnings hit is still building.

And that hit is real. This is not a story where nothing is wrong. Depreciation is climbing fast. Microsoft’s depreciation and amortization jumped 53 percent in a single year, to 34 billion dollars. Amazon's total depreciation and amortization came to 65.8 billion for full-year 2025, up about 25 percent in a single year, and it keeps climbing as more of that capex lands on the income statement. Claude Code pulled the balance sheets to show why: Microsoft’s property and equipment grew by 69 billion dollars in one year, and Amazon’s AWS assets nearly doubled. All of that is only now starting to depreciate.

But here is the part that flips it. The worst of the drag is ahead, not behind, because capex is still growing, so depreciation keeps rising for two to three more years before it peaks. The fear that crushed these stocks was about the cash. The real cost is the depreciation. And depreciation is temporary next to how long the assets earn.

Amazon has run this exact movie before, and Jassy says so himself. In the 2025 letter he goes back to 2014, when AWS was deep in its own spending and a senior leader inside the company openly questioned why they were even in the business. The market disliked the spend then too. His point is that long-term bets never travel in a straight line, they zig up, stall, and double back. He borrows a phrase for it: “straight line was a lie.” Then the comparison that lands it. Three years after AWS launched, its revenue run rate was only in the tens of millions. Three years into the AI wave, Amazon says AWS’s AI run rate is already past 15 billion dollars, roughly 260 times larger at the same stage.

In 2006, as Amazon poured money into the infrastructure that became AWS, BusinessWeek ran a skeptical Bezos on its cover under the headline "Amazon's Risky Bet." A Piper Jaffray analyst caught Wall Street's mood: "I have yet to see how these investments are producing any profit." The spending was called a distraction. That distraction is now AWS. Bezos keeps the cover framed.

That is the whole reframe. The cash that looks burned is being converted into what Amazon believes is its next AWS-scale pillar, and the only genuine cost, depreciation, fades as the assets earn.

One honest caveat, because it’s the hinge the whole thing turns on. This holds only if the AI revenue actually shows up. If demand disappoints, that rising depreciation stops being temporary and becomes a years-long drag with nothing behind it. So the question is no longer “why are they burning cash.” It is 'when do these assets start paying, and is the demand really there.' But before I let any of that into the thesis, I ran it through the same check as the first set of numbers.