The Mistake That Cost 12 Months and the System That Fixed It

How the Bank of Japan’s December 19 decision could trigger another yen carry trade unwind

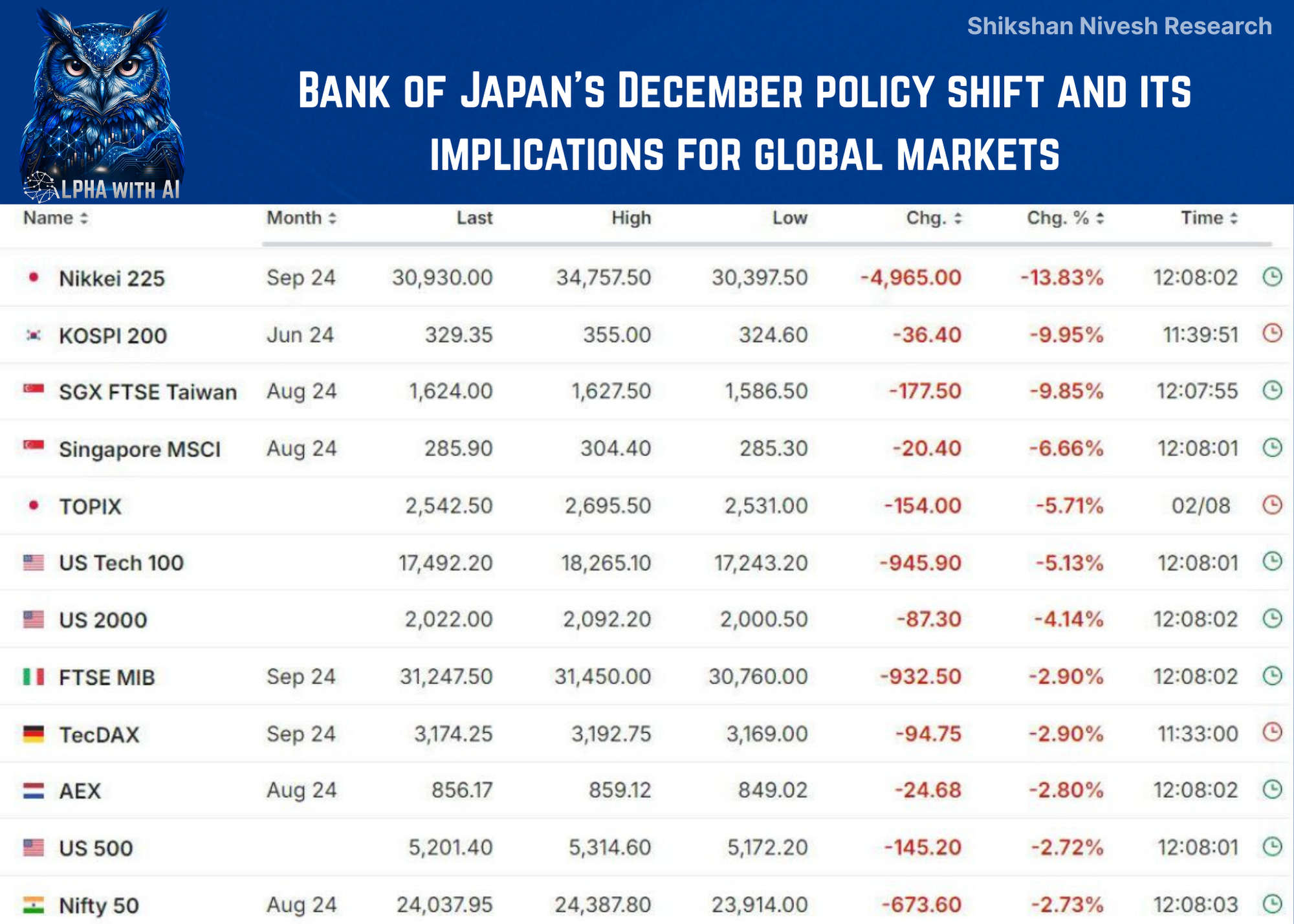

August 5, 2024.

Global markets were bleeding.

Japan: -13%

Korea: -10%

Taiwan: -10%

Nasdaq Futures: -5%

I sent this note to my clients that day: