Research Dive #2: Solstice Advanced Materials (SOLS)

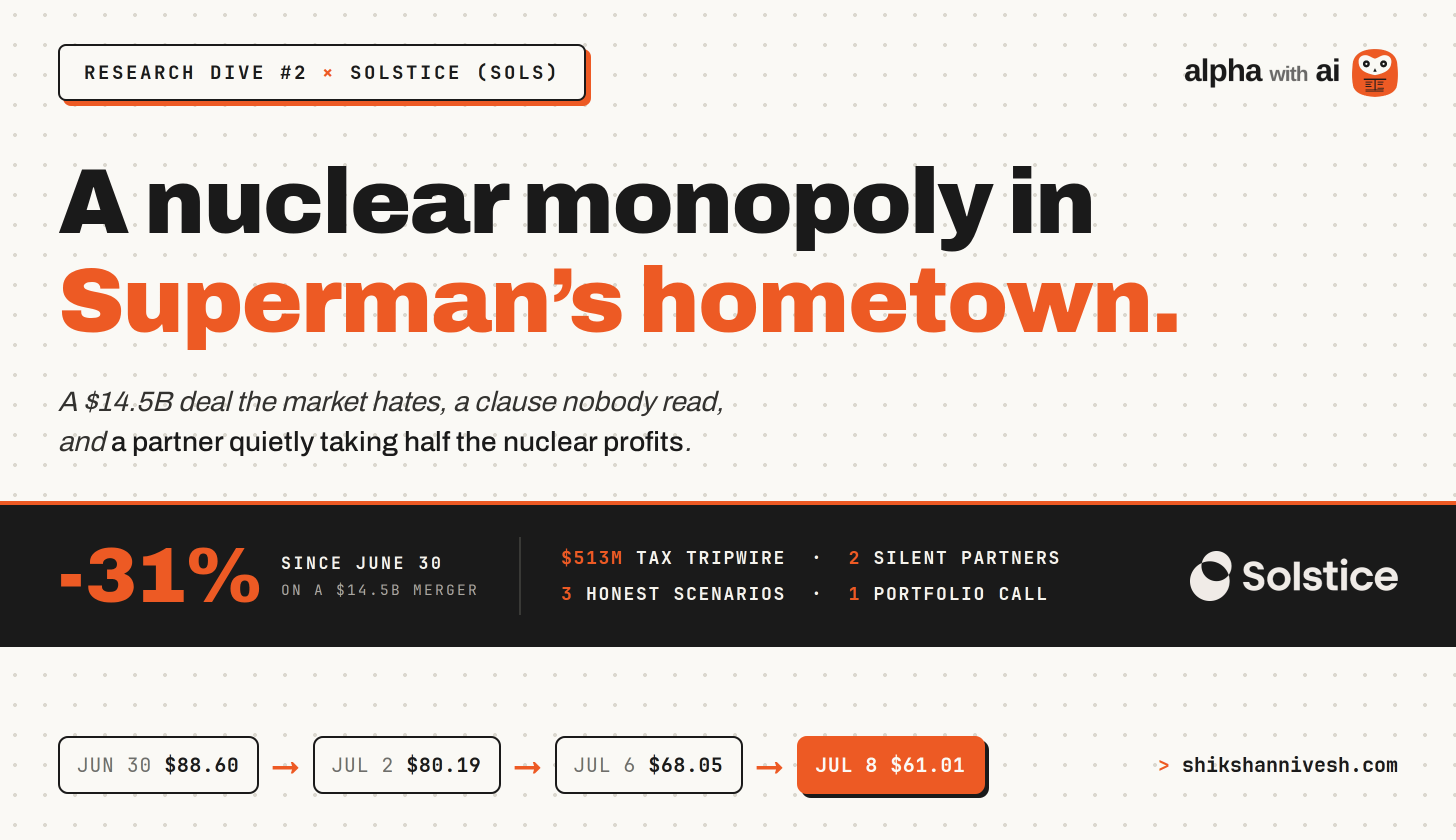

Why is Solstice (SOLS) down 31%? A $14.5B deal the market hates, a $513M Honeywell clause nobody read, a nuclear monopoly in Superman's hometown & a silent partner taking half its nuclear profits.

On the banks of the Ohio River in southern Illinois sits a small town with a fifteen-foot bronze Superman in its square. The town is called Metropolis, and it has been officially calling itself his hometown since 1972.

Metropolis has a second claim almost nobody knows, and it is better than the first.

On the edge of town sits the only commercial plant in America that can take mined uranium and turn it into the gas every enrichment facility needs before it can become reactor fuel. Not the biggest such plant. The only one. Every American plan to build more nuclear power, every promise to feed AI’s appetite for electricity with reactors, every law weaning the fuel supply off Russia eventually runs through one industrial site in Superman’s town. The place famous for a hero who draws his power from the sun quietly runs on uranium. (No, they do not make kryptonite. I checked the product list.)

The town square celebrates a fictional man who could split atoms with his bare hands. The industrial park quietly feeds the machines that split real ones. Tourists photograph the statue every day. Nobody photographs the plant.

For decades nobody photographed the company either. The plant was buried inside Honeywell, one conglomerate asset among hundreds, filed somewhere between cockpit computers and thermostats. But conglomerates went out of fashion. Investors decided they would rather buy their businesses one at a time, priced one at a time, seen one at a time. So in October 2024 Honeywell started taking itself apart, announcing it would spin off its advanced materials business, and within months the whole empire was slated to split in three. The pitch, repeated in every breakup of the last decade: let each business finally be seen clearly.

Being seen clearly. Hold on to that phrase. It is the entire point of this story.

The chemicals business took the name of its own refrigerant brand, Solstice, and on October 30, 2025, Solstice Advanced Materials began trading on its own. And what walked out of that divorce is the most mild-mannered business you could invent. The gas inside your air conditioner. The film sealed over the pill you swallowed this morning. A featherweight fiber that stops bullets for a living and never once brings it up at parties. Clark Kent, incorporated in Delaware. Except this Clark Kent owns the plant in Superman’s town, and for eight months, almost nobody looked twice.

Then came the reveal. On June 4 this year, management held a webinar for one purpose: to show the world the nuclear business. Bank analysts dialed in with questions. The story started traveling. Therefore the stock climbed, and by the end of June it closed at $88.60, within a few percent of its high since the spin. The glasses were coming off, and the crowd was gasping on cue.

But thirty-two days after the reveal, on July 6, the same management announced a $14.5 billion agreement to acquire Element Solutions, an electronics chemicals company, paid for in cash it is borrowing and shares it is printing.

The crowd did not gasp. It ran. Down 15 percent on announcement day, by my math from the daily closes. Down 31 percent from that June close by Wednesday, $88.60 to $61.01, before clawing back to just under $63 as I write this. Type “why is SOLS stock down” into a search bar that week and every answer said some version of the same thing: dilution, debt, a company barely out of the wrapper betting itself on a mega-deal.

So here is the whole five weeks, drawn as the comic strip it secretly is. Panel one: the mild-mannered chemicals company steps out of the phone booth, cape visible, crowd gasps. Panel two: the crowd falls in love. $88.60. Panel three: the hero announces he is spending $14.5 billion, mostly borrowed, on a second costume. Panel four: tomatoes.

Panel five is still blank. Either Metropolis is watching its superman get booed for doing something heroic, or it just watched a man in a costume promise to fly.

The CEO went on CNBC the evening of the announcement, called it a generational growth opportunity in semiconductors and advanced electronics, and blamed the selling on hedge funds running merger arbitrage (funds that trade the gap between deal terms and market prices, not the business itself). The sellers did not go on television. Sellers never do. Panel five does not get drawn on television at all. It gets drawn in the filings.

So I pointed Claude Code at EDGAR and had it pull the entire paper trail of an eight-month-old public company: the merger agreement, the spin-off information statement, the tax agreement Honeywell still holds over its former child, both companies’ annual reports, every 8-K since the separation.

(The rig doing this work, Claude Code running inside Obsidian with every filing it pulls saved into the vault, has its own editions: how I set up Claude Code as my investment research analyst, and the 2.0 rebuild that moved everything inside Obsidian. Start there if you want to run this yourself.) And I gave it one instruction before anything else: build the case against this company before you let me like it.

What came back includes a number I have not seen in a single headline about this deal. It sits in the termination fees of the merger agreement, it is $513 million, and it explains why this deal is shaped the way it is shaped, why the terms could not bend while the stock fell, and why Honeywell, eight months after the divorce, is still in the room.

Hold that. It gets its own section.

And hold the plant in Superman’s town. Because the strangest part of this story is not the deal everyone is arguing about. It is the asset almost nobody was pricing before the argument started.

First, the company itself. I promise you touched its products this week without knowing it.

That, after all, is what mild-mannered means.

Quick context before we go in. I build the AI research workflows I wish I’d had on the equity desk, then show you exactly how they run on real companies. Free to join ~5,000 investors reading along. Subscribe and the next one lands in your inbox.*

THE 60-SECOND THESIS

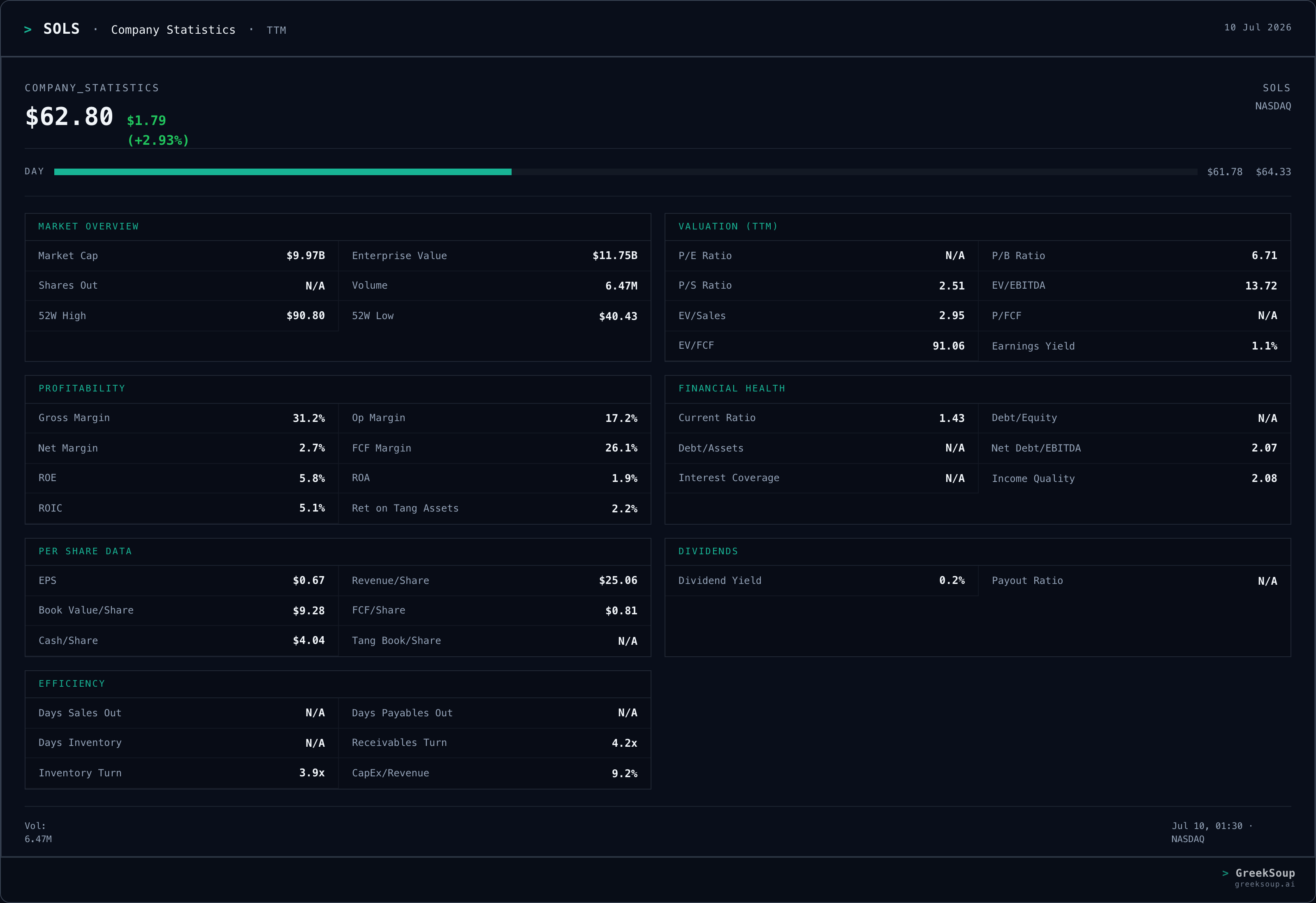

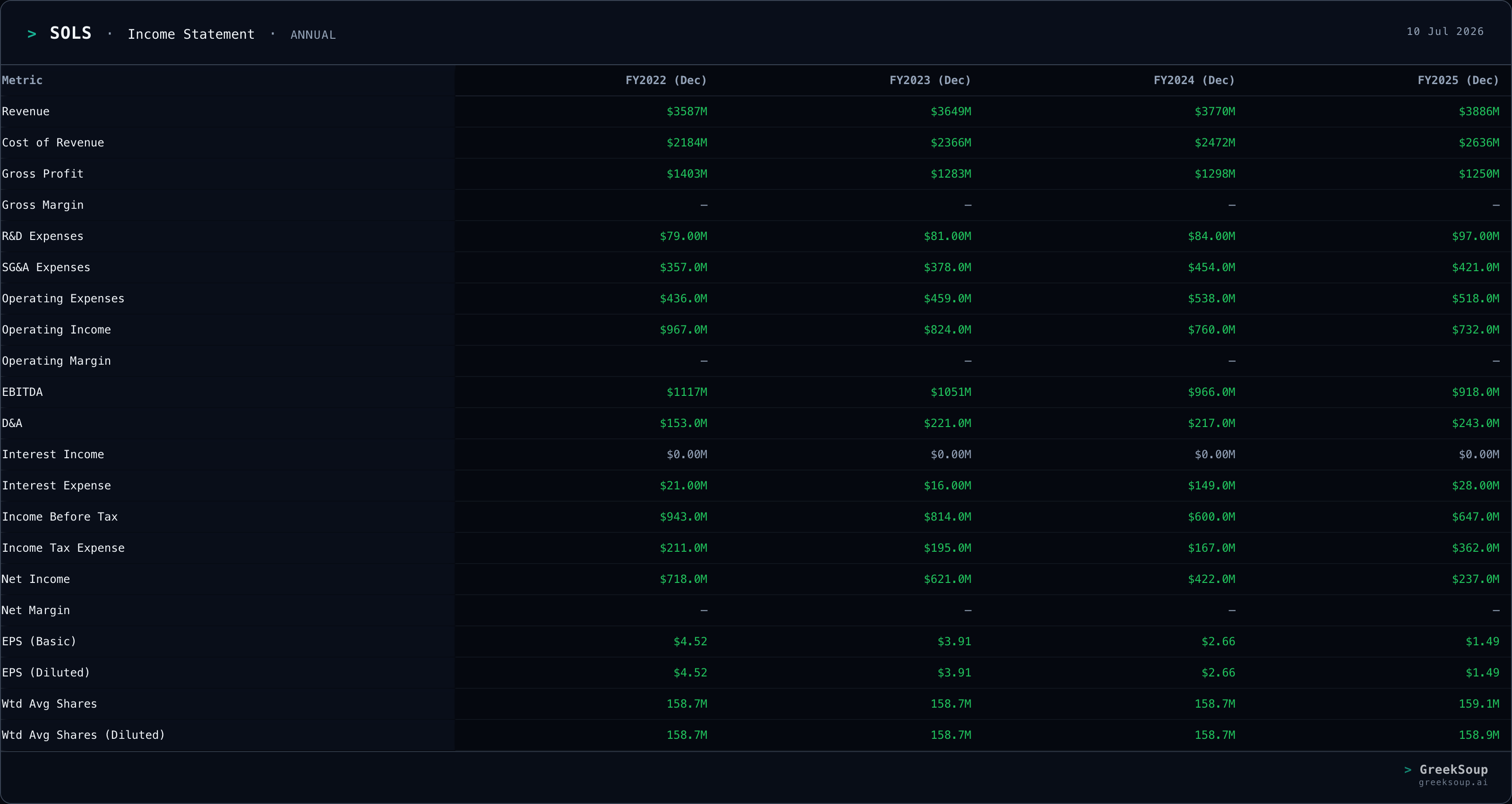

What they do. Solstice sells $3.9 billion a year of chemistry most people touch daily and never see: refrigerant gases for air conditioners (the largest line, $389 million in the first quarter alone), high-barrier film for pharmaceutical packaging, bullet-stopping fiber for armor, ultra-pure materials for semiconductor fabs, and uranium conversion for the nuclear fuel cycle, through the only plant in America that can do it. Two reporting segments: Refrigerants & Applied Solutions, the bigger one, earning 35 percent EBITDA margins last year and 39 the year before, and Electronic & Specialty Materials at about 18. The whole company earned $957 million of adjusted EBITDA last year at a 24.6 percent margin, and until July 6 it carried a clean balance sheet: about 1.4 times net leverage (net debt divided by yearly EBITDA, meaning how many years of profit it would take to repay the debt).

Why it is down. On July 6, management agreed to buy Element Solutions, an electronics chemicals company, for $14.5 billion including its debt. To see what the market flinched at, look at how the bill gets paid. Each Element share receives $10.00 in cash plus half a Solstice share. The cash half is borrowed: a $4.7 billion bridge loan from Goldman Sachs, which takes Solstice from owing about 1.4 years of its profit to owing roughly 3.5 years of it at close. The share half is printed: enough new stock that Element’s owners will hold roughly 44 percent of the combined company. If you owned a slice of Solstice in June, this deal hands nearly half of every future dollar of profit to somebody new, and it borrows three and a half years of earnings to do it. One more mechanical detail did quiet damage all week: the share ratio is fixed. Half a Solstice share is the payment whether the stock trades at $88 or $61, so every dollar the stock falls also shrinks what Element’s holders get paid, and hedge funds trade that shrinking gap mechanically, selling Solstice as they go. That is the arbitrage the CEO complained about on television. The skeptics also have real cracks to point at: the flagship segment’s profit margin fell 522 basis points (a basis point is a hundredth of a percent, so that is a drop of about 5 percentage points) in the first quarter, and 1,225 basis points, more than 12 full percentage points, in the quarter before that. Management’s explanation, in the filings, is product mix: the market is shifting from the old high-margin refrigerant gas to its replacement faster than the replacement’s economics have matured, and that shift more than offset favorable pricing. Put simply, a company eight months out of the wrapper asked the market for $14.5 billion of trust, paid with borrowed money and freshly printed shares. The market said no, erasing $4.1 billion of value in six sessions.

Why I think the selloff may be aiming at the wrong target. Everything the market punished last week sits on one side of the company: the deal, the debt, the dilution. The assets sit on the other side, and they did not change. The nuclear business grew 27 percent last quarter and already holds $2.2 billion of signed future orders, roughly five years of work at its recent pace of about $430 million a year in sales, at the only plant in the country that can do the job, while Washington orders more of exactly this capacity and shares the cost of building it. The Electronic Materials line grew 19 to 21 percent selling into semiconductor plants. These are the two fastest-growing things Solstice owns, and neither one appeared anywhere in July’s argument, which was entirely about the bill. So here is the hinge this edition turns on, in one question: can the boring cash engines, the refrigerants protected by a federal quota law and the uranium work already under contract, keep paying the new mortgage while the exciting semiconductor story proves itself out? If yes, the market just repriced the costume and forgot the cape. If no, then three and a half years of debt on a one-year-old company is exactly as dangerous as July says, and the sellers are right. There is also a wrinkle in how the nuclear profits get shared that I have not seen anyone mention, and it cuts against the easy bull case. Panel five has more than one way to end, and I will draw it honestly.

What could turn it. The deal proxy (the S-4, the filing that must precede the shareholder votes) will publish the boards’ projections and bankers’ math within months. Deleveraging is promised below 3 times within 18 months of closing, and the close itself is expected in the first half of 2027. Old nuclear contracts keep rolling onto today’s far higher conversion prices quarter by quarter. Management has committed $180 million a year of merger synergies by year three. And the company guided 2026 to $975 million to $1.025 billion of EBITDA before any of the deal lands, with the refrigerant quota law tightening the old gas’s supply on a schedule written into statute.

THE BUSINESS IN ONE LENS

Every screener on earth files Solstice under specialty chemicals. Fair enough. But read the annual report end to end and a stranger pattern starts repeating, and once you see it, you cannot stop seeing it.

Almost nothing this company sells is protected mainly by chemistry. It is protected by permission.

The refrigerants business, the largest by far, lives inside a regulatory transition: governments in the US and Europe are steadily retiring the old generation of gases and steering the market toward the low-warming replacements that Solstice builds and brands. The 10-K says the quiet part in plain text: these markets provide “regulatory protection for incumbent producers.” The nuclear business runs the one facility in the country with the license and the capability to do its job, and the same 10-K states that in a single sentence: “the sole domestic facility producing uranium hexafluoride gas.” Even the smaller lines live behind walls. The healthcare film is being joined by a medical-grade propellant certified for inhalers. The fiber sells into government armor programs. None of this is shampoo. You cannot decide to compete with most of this company by raising money and building a factory, because the factory is not the barrier. The paperwork is.

Honeywell did not spin off a chemicals company. It spun off a collection of permissions. And permissions are the hardest thing on earth to replicate, which is precisely why the market’s five-day verdict deserves a second look.

Now put numbers on the lens, because a lens without numbers is a slogan. Solstice reported $3,886 million of sales last year, split into two segments but really three engines.

Engine one, the transition machine. Refrigerants did $1,511 million of sales last year, up 16 percent, and grew 19 percent again in the first quarter. Here is the tension that will decide the hinge: the same regulation that guarantees demand for the new gas is currently squeezing profitability, because the market is shifting toward the replacement faster than its economics have matured. Management calls this product mix. The segment’s margin fell from 38.9 percent to 35.2 percent last year, and the market reads that slide as decay. Whether it is decay or a toll paid once is, I think, the single most important question in the stock, and it gets its full treatment when we reach the hinge.

Engine two, the tollbooth in Superman’s town. Nuclear did $356 million of sales last year, and here honesty requires an ugly detail the bulls skip: that was DOWN from $446 million the year before, because this is a business of lumpy multi-year contracts and delivery schedules, not a smooth subscription. The momentum now runs the other way, 27 percent growth last quarter, $2.2 billion of signed orders, and a Department of Energy agreement to share the cost of expanding the plant. One more detail, and hold it for the payoff later: Solstice does not pocket this tollbooth alone. The plant sells every kilogram through a joint venture, half-owned by a partner almost nobody discussing this stock has mentioned. What that does to the easy math is a payoff that comes after the paywall, and it is worth the wait.

Engine three, the quiet growth line. Electronic Materials did $409 million of sales last year and grew 19 to 21 percent in the recent quarters, selling ultra-pure materials into semiconductor plants, the end of the AI buildout where money is being spent fastest. (I rebuilt that spending from the hyperscalers’ own filings in is big tech’s AI capex mispriced; this is the shovel-seller’s corner of that story.) It sits inside the second segment with research chemicals and the armor fiber, which together add another $687 million.

Step back from the three engines and read the whole machine in one breath. The first segment earned $981 million of EBITDA at a 35 percent margin. The second earned $203 million at 18.5. Corporate costs ate $184 million, and the company poured $408 million into capital spending, up 38 percent, most of it aimed at the nuclear expansion and the growth lines. The balance sheet, before the deal: $2.0 billion of debt against $642 million of cash, about 1.4 times EBITDA. Modest. Boring, even.

Which brings us to the honest question this lens leaves hanging. If the permissions are so valuable, why did profit fall while revenue rose for a fourth straight year? The answer is not one thing, and the market’s five-day verdict treated it as one thing. Untangling it is the next section, because the bear case here is real, filed, and worth respecting before I argue with it.

WHY IT’S DOWN

The bears did not invent this selloff, and pretending otherwise would insult both them and you. Here is their case at full strength, every piece of it from the filings.

The earnings a screener sees are genuinely ugly

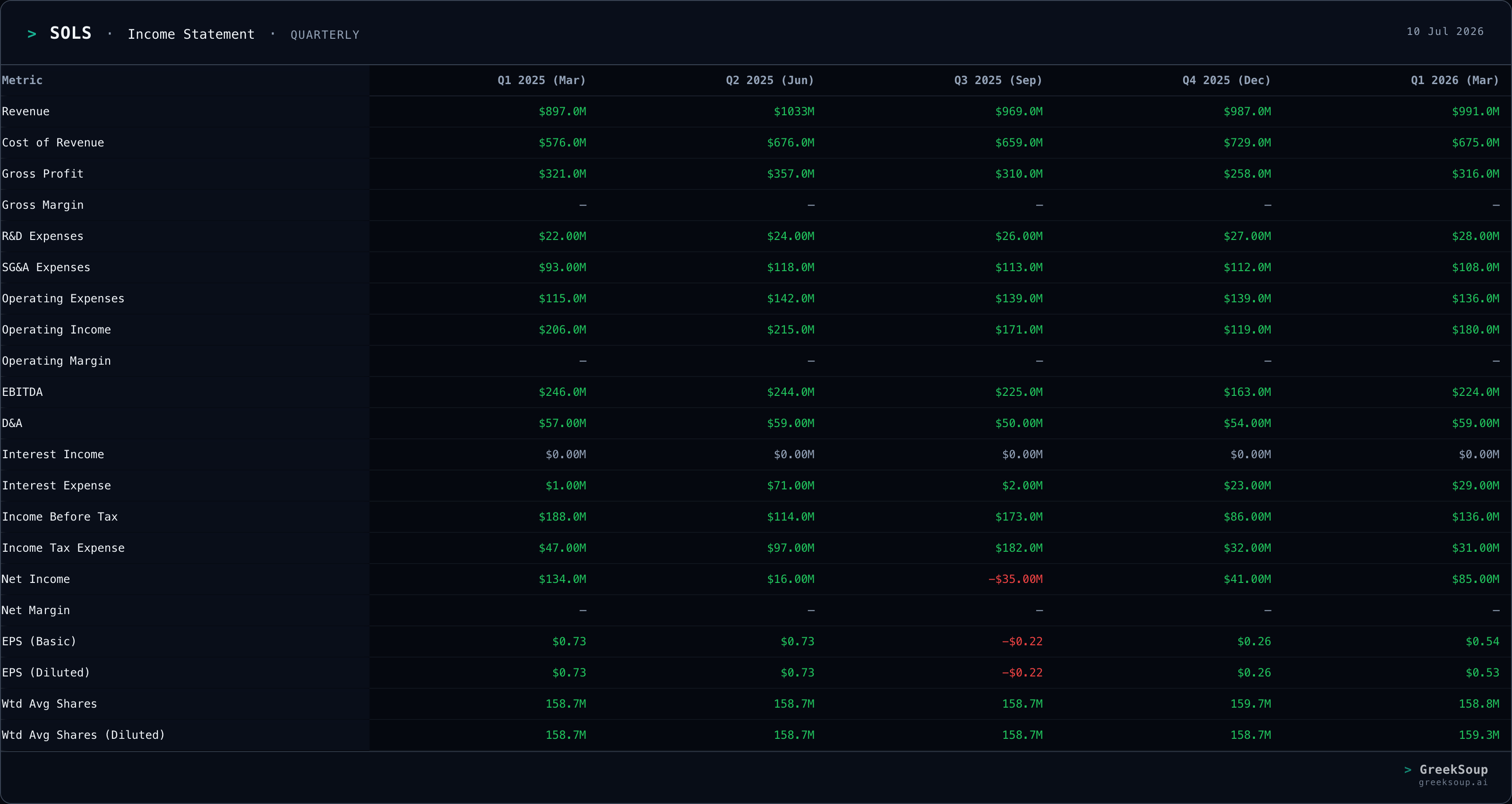

Net income fell 53 percent last year, from $605 million to $285 million, and the share attributable to Solstice’s own holders fell 60 percent. The filings show exactly where it went: transaction-related costs more than quadrupled to $117 million, the effective tax rate jumped from 24 percent to 56 percent in the spin year, and interest costs doubled. Some of that is the one-time price of being born as a public company. Not all of it. And there is a quieter line in the same table that should bother bulls more than the tax rate: last year’s 3 percent revenue growth came entirely from price and currency. Volume contributed zero.

The flagship’s margin is walking downhill in the middle of its transition

The refrigerants segment earned a 39 percent margin two years ago, 35 percent last year, 34.1 percent in the first quarter, and the fourth quarter of 2025 printed a 12-point year-over-year drop. Management’s filed explanation is product mix: customers are moving to the new low-warming gas faster than its economics have matured. The bear translation is blunter. The old gas was the profit engine, regulation is retiring it on a schedule, and the replacement has not yet proven it can earn what the original earned. A transition that guarantees demand does not guarantee margin.

The crown jewel just had a down year

The nuclear line everyone got excited about in June did $356 million of revenue in 2025, down from $446 million in 2024. Multi-year contracts deliver in lumps, and a down year proves nothing by itself, but it kills the tidy story that this asset only goes up. Whoever buys the tollbooth story has to hold it through delivery schedules that wobble.

The passengers are heavier than they look

The two growing engines carry the rest of the train. Healthcare Packaging fell 25 percent in the fourth quarter, which the filings attribute to customers destocking and the factory under-absorption that comes with it (a plant built for full production gets more expensive per unit when volumes drop). Building Solutions & Intermediates, the construction-linked line, fell 5 percent in the fourth quarter and 8 percent again in the first. Corporate costs rose to $184 million. None of these is a thesis-breaker alone. Together they mean the growth engines are pulling passengers, and the market noticed.

The screeners never stood a chance

Here is a mechanical reason the selling fed on itself. On last year’s reported earnings of $1.49 a share, June’s peak price was nearly 60 times earnings, so every quantitative screen on Wall Street filed Solstice under “wildly expensive chemicals company.” That earnings figure is polluted by the spin: the one-time transaction costs and the 56 percent tax year sit inside it. On management’s own adjusted guidance of $2.45 to $2.75 for this year, the price as I write is closer to 24 times. But a screen does not read footnotes, a one-year-old company has no long record to overrule the screen, and when the deal headline hit, the machines had no reason to hesitate.

A fish swallowing a fish its own size

Step back to the simplest number of all. On the day before the announcement, all of Solstice’s shares together were worth about $12.7 billion. The deal it signed is $14.5 billion including assumed debt. This company is buying something priced at more than the entirety of itself, and the promised reward, $180 million of annual synergies by year three, works out to about 1.2 percent of the purchase price. Deals this large relative to the buyer leave no room for integration error, and the buyer has been integrating itself for only eight months.

The seller prepared for this sale

Element Solutions is not a distressed seller. Its founder and chairman, Sir Martin Franklin, one of the most experienced dealmakers in the industry, signed a voting agreement supporting the deal the day it was announced. Five months earlier, Element had quietly upsized its own credit facilities, adding $450 million of term loans and a new $500 million revolver. None of this is improper, and none of it is comforting either: an eight-month-old management team is buying what a thirty-year dealmaker is selling, at a 15 percent premium.

And Solstice must close, whatever the weather

Read the merger 8-K closely and one absence matters: financing is not a condition of the deal. The $4.7 billion bridge is a 364-day loan, the permanent replacement will be a term loan and bonds at a rating the company itself describes as sub-investment grade, and if credit markets are ugly when the bill comes due, Solstice’s obligation to close does not care. The deal’s end date runs to July 2027, extendable into 2028, which means the arbitrage pressure on the stock has a very long runway. The proxy statement with the boards’ own projections has not even been filed yet. The market is pricing a deal whose interior nobody outside the boardrooms has seen.

Add it up and this is a coherent, filed, honest bear case: earnings down, margins compressing, the star asset lumpy, the smaller lines bruised, a deal bigger than the buyer, a shrewd seller, a must-close obligation, and a trust deficit that a company eight months old has not had time to earn its way out of. The market did not panic over nothing.

But notice what the market did NOT have during those five sessions: the paperwork underneath. The proxy with the boards’ projections does not exist yet. The merger agreement’s fine print, where that $513 million number from the top of this piece lives, went largely unread. And buried in the annual report’s investment note is something I have not seen in a single writeup of this company: a second quiet stakeholder, inside the nuclear business itself, collecting a share of the profits everyone spent June celebrating. The bears priced what they could see. The rest of this edition is about what they could not.

The paid half starts here. In it: the hinge, whether the quota-protected refrigerant engine and the uranium tollbooth can pay for this deal. The fine print, from the $513 million tripwire to the uncounted partner inside the nuclear profits. What I think the stock is worth, in three honest scenarios with the method shown. And where I land, as a real decision in the live model portfolio that comes with every dive for paid subscribers. Position one was Accenture. This edition decides position two.