Claude Code Read Elon Musk's 277-Page SpaceX Prospectus So I Didn't Have To

How to use Claude to interrogate any IPO prospectus, using SpaceX as the test case, whether it's your first filing or your hundredth.

A reader messaged me last week and asked if I’d break down the SpaceX IPO.

I almost said no. Not because it isn’t interesting. Because I don’t write about whatever is trending that week. Trends rot. In AI especially, the hot thing today is stale in three days, and I’m not interested in teaching you something with a shelf life. I write about workflows that still matter a year from now, and I usually find them buried in messages like this one, from readers telling me what they’re actually stuck on.

This one was worth it. Because SpaceX isn’t really the lesson. The lesson is the document.

I’ve admired this company for years. Not Musk the personality. The work ethic, the engineering DNA. There’s a story about how that DNA works that has stuck with me for a long time.

An engineer comes to Musk and says he needs to buy a part. It costs $1,200. Musk doesn’t ask why they need it. He asks what it’s made of. Some kind of metal, they say. He asks what that metal costs. They check the London Metal Exchange. Fifty dollars a kilo. He just looks at them. And eventually the room works out what he already knows, that the $1,200 part is maybe $300 of raw material and they should build it themselves.

That’s the whole company in one scene. He refuses to accept the price he’s handed. He breaks it down to the raw inputs and rebuilds the real number from scratch.

Every competitor knows this story. None of them have the DNA to actually do it. That refusal is why these companies trade at a premium nobody else gets, and why Wall Street bends the knee.

So here is what I find funny.

The man who has never accepted a sticker price in his life just handed the public a 277-page sticker price. The SpaceX prospectus. Plus a hundred-page addendum. Dozens of photos of rockets going into orbit. A soaring story. And somewhere inside all of it, the five or six numbers that actually decide whether this is the business of a generation or the most expensive story ever sold to retail.

Twenty years ago a prospectus was short. You could read one in an evening and know what you owned. Today they run two to three times longer, and not because there is two to three times more worth knowing. The length is the point. Noise is a great place to hide signal.

I’m not going to read 277 pages to find five. Not in 2026. Time is the only thing I can’t get back, and there is no reason left to spend it this way.

So I did to the prospectus what Musk would do to that $1,200 part. I refused the price. I broke the document down to its raw inputs and rebuilt the real number myself.

This is how. And it works on any prospectus, any annual report, any 300-page document built to wear you down, whether you’ve been investing for years or you’re about to analyse your first IPO.

One thing before we start. The title says Claude Code, and if that sounds like a developer tool you’re about to be locked out of, relax. There’s a no-terminal version of this exact workflow, same power, no commands, and I’ll show you both. Nobody gets left at the door.

Almost everything I make ends up here, in the open, because a workflow you can’t see doesn’t make anyone a better investor. The paid tier exists for the readers who want the skills, the prompts, and the downloadable guides the moment they ship, and it’s quietly what keeps me doing this instead of something that pays better. If you’re one of them already, thank you. If you’re not, no wall here. This one’s yours, all of it.

DATA IS NOT INFORMATION

Aswath Damodaran has a framing in his recent SpaceX note I keep coming back to. He calls it data versus information. The way I've come to interpret it for myself is simpler. Data is not information.

A prospectus is full of data. Page after page of it. Numbers, disclosures, risk factors, diagrams. What it is short on is information, the small number of things that actually change what you believe about the business. Damodaran has even written a paper on this. Prospectuses today run two to three times longer than they did three or four decades ago, and not because companies have three times more worth telling you. The extra length is mostly defensive. Risk factors written to be unfalsifiable. Language vetted so nothing in it can be used against the company later.

So before I open any filing, I do something that sounds backwards. I read what other people wrote about it first.

Here is why. I love reading. I will happily spend an evening with a great piece of writing about a business. But there is a difference between reading an author and reading a document. An author I respect is accountable to their own reputation. They have a name on the page and a track record you can check. A prospectus is written by lawyers who are accountable to one thing, protecting the company that pays them. Given the choice, I will read the author first, every time. Not because the author is always right. Because the author is trying to inform me, and the document is trying to sell me.

So that is where I started with SpaceX.

READ THE AUTHORS BEFORE THE DOCUMENT

I started with Aswath Damodaran.

He had just published a post-prospectus update on SpaceX, revisiting a valuation he’d first attempted before the filing came out. This is exactly the kind of reading I trust. A man who has valued more companies than almost anyone alive, showing his work, telling you what he got wrong the first time and what the prospectus changed. I read it once for the story and once for the numbers. Then I clipped the whole thing into my Obsidian vault so it sits in my own research library, searchable, permanent, mine. If you want the setup that does this, I’ve written about how my research library works before which you can read here.

Then I went to X.

Not for hot takes. X has the largest live investing community on earth, and buried in the noise are people who have actually done the work and published their reasoning. I asked Grok to pull me the most substantive bull cases and, just as deliberately, the most substantive bear cases, with names and links so I could read the originals myself. I did not want a summary that hid the disagreement. I wanted the strongest version of both sides. I clipped the results into Obsidian alongside the Damodaran piece.

A note on this, because it matters. Everything I gathered at this stage is opinion. Smart opinion, sometimes. But opinion. None of it is a fact until I have checked it against the filing. A bull who tells you Starlink subscribers doubled is giving you a lead, not a number. The number lives in the prospectus, and that is the only place it counts.

Now I had a folder full of intelligent people arguing about SpaceX. And only then did I open the prospectus itself.

That is the order that matters. Authors first, to build the story and the questions. The document last, to settle them.

THEN I OPENED THE PROSPECTUS

So I opened it. Two hundred and seventy-seven pages, plus a hundred-page addendum. Dozens of photographs of rockets leaving the atmosphere. A story about humanity becoming multiplanetary, written to make you feel something before you’ve read a single financial statement.

I read enough to confirm what Damodaran already warned me about. The signal is in there. It is just buried under a great deal of material that exists to fill pages, not to inform a decision. Risk factors that could apply to any company on earth. Sentences engineered by lawyers to mean as little as possible while technically disclosing something.

And here is where I made my decision. I was not going to read all of it.

Not because I couldn’t. I’ve read plenty about this company over the years and enjoyed every word of it. But there is a difference between reading and grinding. Reading 277 pages of mostly noise to find five pages of signal is not analysis. It is a tax on my time, and time is the one input I never get back.

Think back to the engineer and the $1,200 part. Musk didn’t refuse to understand the part. He refused to overpay for it. He broke it down to the raw metal and rebuilt the real cost himself. That is exactly the move here. I’m not refusing to understand the prospectus. I’m refusing to overpay for it in hours. So I broke it down to its raw inputs and let a machine do the reading that a machine should do.

I clipped the entire prospectus into the same Obsidian vault that already held Damodaran’s piece and the bull and bear cases from X. Then I pointed Claude Code at the vault Or its no-code twin, if a terminal isn’t your thing. More on that in a second.

This is where the actual work begins. And this is the part that works on any document you ever have to analyse, not just this one.

THE WORKFLOW: REFUSE THE PRICE, REBUILD THE NUMBER

A quick word on setup, because I’ve covered it in full before and won’t repeat all of it here. Pick your path, then come back.

If you’re using Claude Code, it’s not a coding tool. It’s Claude with hands, the same Claude you talk to in the chat window, except this version can read the files on your computer. I run it inside Obsidian, pointed at the vault where I just clipped the prospectus. If you’ve never wired this up, I walked through the whole thing in how I set up Claude Code as my investment research analyst. Start there.

If a terminal isn’t your thing, use Claude Cowork instead. It’s the same agentic engine in a friendlier room, no commands, you just point it at a folder and ask in plain English. I’ve shown exactly how I use it for a full equity report before, in how I used Claude Cowork to write a full equity research report in 90 minutes. Same destination, gentler road.

Whichever path you’re on, the rest of this works identically. The prompts are the same. Only the room changes.

One caution for both. Give the tool a folder with a copy of the prospectus in it, not your entire vault, and never your whole drive. These agents can edit and delete files, so you fence them into a sandbox and let them work there.

Now the work. I don’t ask the prospectus open-ended questions. I run it through the same checklist I run on every idea, in the same order, because the order is the discipline. Skip ahead to valuation and you’ll talk yourself into anything.

STEP ZERO: THE FIVE-LINE TEST

Before any number, one human question. Can I explain this business in five lines to a ten-year-old? If I can’t, it’s outside my circle and no spreadsheet will save me.

Here’s the honest answer for SpaceX. It’s three businesses wearing one ticker. A rocket business that launches things into space cheaper than anyone else. A satellite internet business, Starlink, that beams broadband down from those rockets. And an AI business, xAI, that runs enormous computers. The first two I understand. The third is where it gets hard, and that’s worth admitting before I read a single figure.

That admission shapes everything. A company you can’t fully explain in five lines isn’t disqualified. But it raises the bar on what the filing has to prove.

Know someone about to buy into an IPO because the story sounded good? Send them this before they do. That’s who it’s for.

THE FRAMEWORK, AND WHY THE PROMPT IS NOT THE POINT

Here is the part most people get wrong. They go looking for the perfect prompt to paste. But a prompt you copy only works on the company it was written for. What you actually want is the thing underneath the prompt, the question, and the thing underneath the question, the principle. Get those right and you can write the prompt yourself, for any company, forever.

So here is the whole framework in one breath. Every step is a principle. Each principle becomes a single question. Each question becomes one tightly worded prompt that forbids the machine from guessing. The order is fixed on purpose. Growth first, then cash, then debt, then the quality of the profit, and valuation last, always last, because if you let yourself peek at the price before you’ve checked whether the profit is real, you will reverse-engineer a reason to like it.

Five principles, in order:

Is revenue genuinely growing, across years, not one good quarter dressed up as a trend.

Can the business fund its own growth from its own cash, or does it survive on outside money.

Is the debt load sane, or has the company handed control to its lenders.

Does the reported profit show up as real cash, or only on paper. This is the one that catches frauds.

And only now, after all of that, is the price sane?

The pattern of every prompt never changes: tell the machine exactly where to read, forbid it from estimating, demand a page citation for every number, and make it say “not disclosed” out loud when the filing stays silent. A filing’s silences are information too.

STEP ONE: REAL SALES GROWTH

Here is the first prompt I gave the tool, against the prospectus in my folder. It’s the same whether you’re in Claude Code or Cowork:

Read the SpaceX S-1 in this folder. From the audited financial statements and MD&A only, not the narrative or risk factors, give me total revenue for each year reported, and revenue broken out by segment (launch, Starlink/connectivity, AI/xAI) for each year. For every number, cite the exact page and statement it came from. If a figure isn’t in the filing, say “not disclosed.” Do not estimate. You can also refer to the Damodaran article, by the way, from the same folder, but take the numbers clearly from the SpaceX S1 only. What it returned:

Total revenue grew across all three audited years: $10.4 billion in 2023, $14.0 billion in 2024, $18.7 billion in 2025. Real, audited growth.

But split it by business and the real picture appears.

Space, the rockets, went from $3,557M to $3,796M to $4,086M. Barely moving, under 8% in the latest year.

Connectivity, which is Starlink, went from $3,869M to $7,599M to $11,387M. Nearly tripled in two years.

AI, which is xAI, went from $2,961M to $2,620M to $3,201M. It went down before it went up.

SpaceX did not grow because of rockets or AI. It grew because of Starlink, almost entirely. The most famous part of the company is the flattest line on the page.

And the AI segment hides something. The filing's own note says the 2023 AI figure is substantially old advertising and subscription money from X, formerly Twitter, recast after the xAI and X Holdings mergers. So when someone sells you explosive SpaceX AI growth, the filing quietly says the segment shrank its first year and is partly relabeled Twitter income.

One honest limit, specific to IPOs: only three audited years exist here. On a mature company you'd want ten before calling a trend. On a first-time filer you take what you get and stay humble.Full output with every page citation:

The question I’m actually asking: is revenue genuinely growing across multiple years, or is this one good year dressed up as a trend? And is the growth real across all three businesses, or is one segment carrying the rest?

STEP TWO: DOES IT FUND ITSELF

The principle: a business should fund its growth from its own cash. If it survives on outside money, you are betting on the market staying generous.

The prompt I gave the tool:

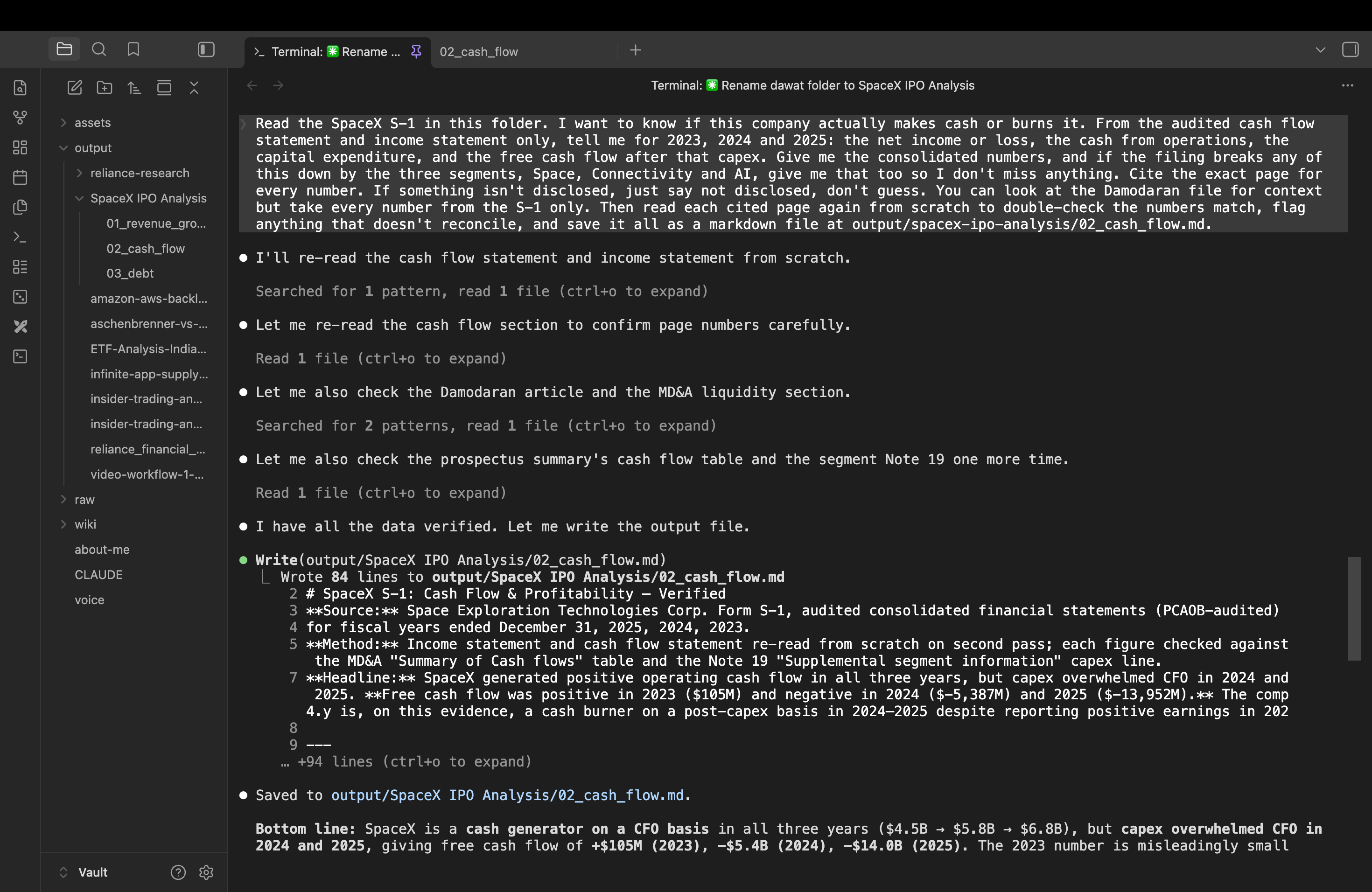

Read the SpaceX S-1 in this folder. I want to know if this company actually makes cash or burns it. From the audited cash flow statement and income statement only, tell me for 2023, 2024 and 2025: the net income or loss, the cash from operations, the capital expenditure, and the free cash flow after that capex. Give me the consolidated numbers, and if the filing breaks any of this down by the three segments, Space, Connectivity and AI, give me that too so I don’t miss anything. Cite the exact page for every number. If something isn’t disclosed, just say not disclosed, don’t guess. You can look at the Damodaran file for context but take every number from the S-1 only. Then read each cited page again from scratch to double-check the numbers match, flag anything that doesn’t reconcile, and save it all as a markdown file.

What it returned:

Operating cash flow, the cash the business throws off before big investment, was positive every year: $4.5 billion in 2023, $5.8 billion in 2024, $6.8 billion in 2025. On that measure the business works.

Then look at what it spends to grow. Capital expenditure went $4.4 billion, $11.2 billion, $20.7 billion. So free cash flow, the cash left after that spending, was a thin positive $105 million in 2023, then negative $5.4 billion in 2024, then negative $14.0 billion in 2025.

So which is it, cash generator or cash burner? It is a cash generator that is choosing to burn cash. Different thing from a cash burner with no choice. SpaceX makes real operating cash, then spends multiples of it building for the future. In 2025 it raised $26.4 billion from outside to fund the gap.

And the segment data shows where the money goes. AI is the black hole. AI capex went from $0.5 billion in 2023 to $5.6 billion in 2024 to $12.7 billion in 2025. More than half of all 2025 capital spending went into AI, the same segment with the smallest revenue and partly relabeled Twitter income.

One number to sit with. In 2025, AI brought in $3.2 billion and consumed $12.7 billion of capex. The business that earns the least eats the most cash.

A note for the careful reader. The 2023 net loss of $4.6 billion looks alarming next to positive operating cash flow. It is not an operating hole. The filing shows the loss is dominated by a $3.8 billion non-cash writedown of the Twitter brand, an accounting entry, not cash leaving the building. A loss on paper and a loss in cash are not the same thing, and the filing lets you tell them apart if you read it instead of trusting the headline.Full output with every page citation:

The question I’m actually asking: can this business pay for its own growth, or is it dependent on the market handing it money every year?

STEP THREE: DOES IT OWE TOO MUCH

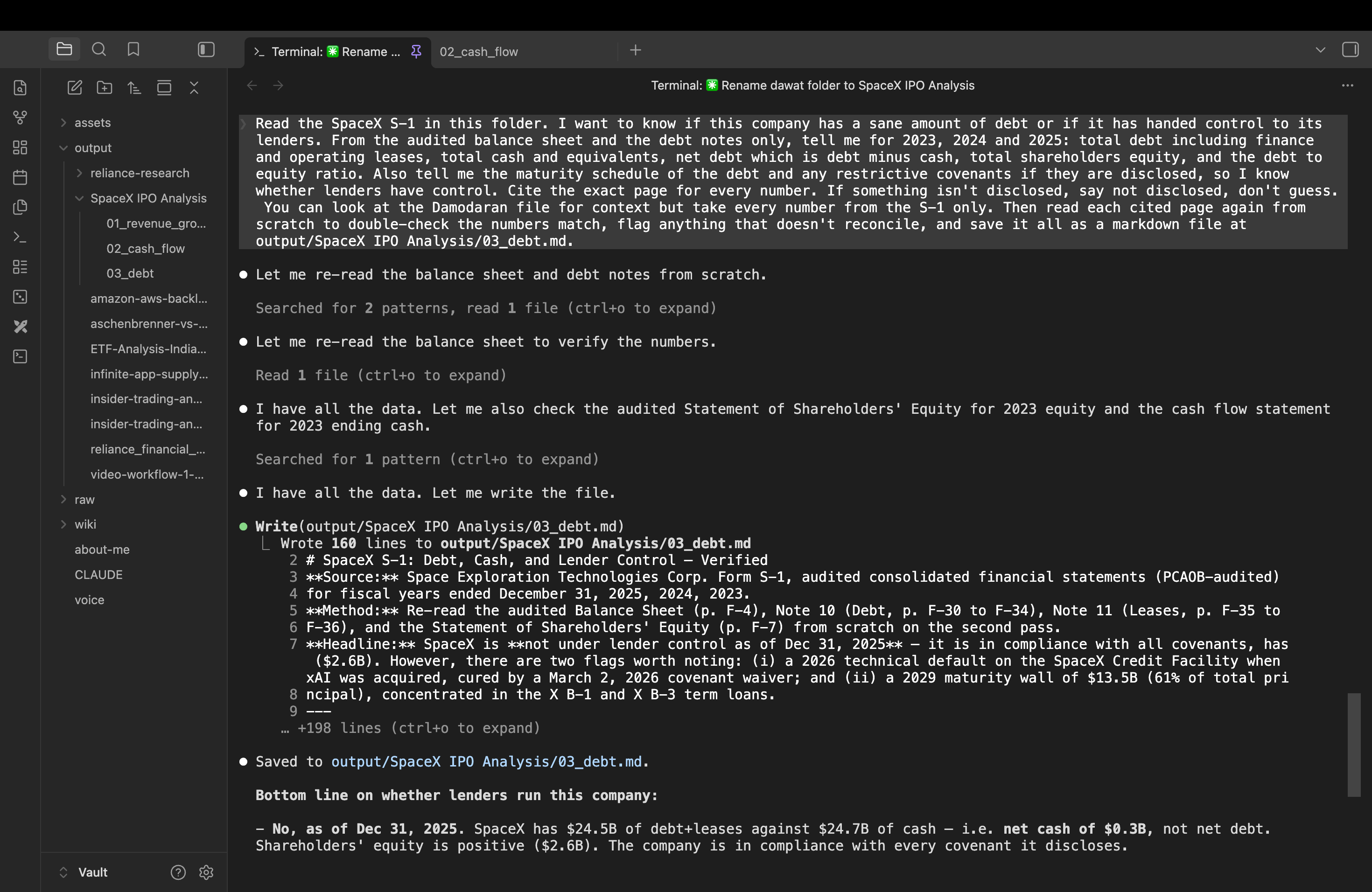

The principle: debt is fine until it isn’t. The question is never just how much, it is whether the lenders are now the ones in control.

The prompt I gave the tool:

Read the SpaceX S-1 in this folder. I want to know if this company has a sane amount of debt or if it has handed control to its lenders. From the audited balance sheet and the debt notes only, tell me for 2023, 2024 and 2025: total debt including finance and operating leases, total cash and equivalents, net debt which is debt minus cash, total shareholders equity, and the debt to equity ratio. Also tell me the maturity schedule of the debt and any restrictive covenants if they are disclosed, so I know whether lenders have control. Cite the exact page for every number. If something isn’t disclosed, say not disclosed, don’t guess. You can look at the Damodaran file for context but take every number from the S-1 only. Then read each cited page again from scratch to double-check the numbers match, flag anything that doesn’t reconcile, and save it all as a markdown file.

What it returned:

The first number looks like a fire alarm. Debt to equity of 9.5 times in 2025, up from 3.2 times in 2024. On its own that screams a company drowning in debt.

It is the wrong read, and this is exactly where a single ratio fools people. The ratio did not jump because debt exploded. It jumped because equity shrank. Shareholders equity fell from $4.9 billion to $2.6 billion, dragged down by the 2025 loss, while the denominator collapsing made the ratio balloon. Debt grew too, but cash grew faster.

Look at it the honest way, net of cash. SpaceX has about $24.5 billion of debt and leases against $24.7 billion of cash. Net debt is negative. The company holds slightly more cash than it owes. On a net basis this is not a leveraged company at all. It is a capital-hungry company funding itself with a mix of debt and equity, and in 2025 it raised $17.9 billion of preferred stock to do it.

So the headline ratio is noise. But reading the actual debt notes, not the ratio, turned up two things no summary would tell you.

First, a default already happened. In February 2026, just after the audited year closed, the acquisition of xAI tripped a technical default on the main SpaceX credit facility. It was cured by a covenant waiver on March 2, 2026. The company is in compliance now. But a fresh default that needed a lender’s permission to fix, weeks before filing to go public, is the kind of thing that lives on page F-30 and nowhere in the headlines.

Second, a wall is coming. More than 88 percent of all debt principal comes due in 2029 and 2030. A single year, 2029, carries $13.5 billion of it, 61 percent of the total, concentrated in loans carrying double-digit interest rates. The near years are quiet. The cliff is loud, and it is dated.

And one tell about the cost of this money. The exit penalties to prepay the xAI debt run between 103 and 106 percent of principal, and one tranche of leases carries a 22.6 percent discount rate. This is expensive money. The company is not under the lenders’ thumb today, but it is paying like a borrower the lenders consider risky.Full output with every page citation, the maturity schedule, and the covenant detail:

The question I’m actually asking: is the debt sane, or has the company quietly handed its future to whoever holds that 2029 maturity wall?

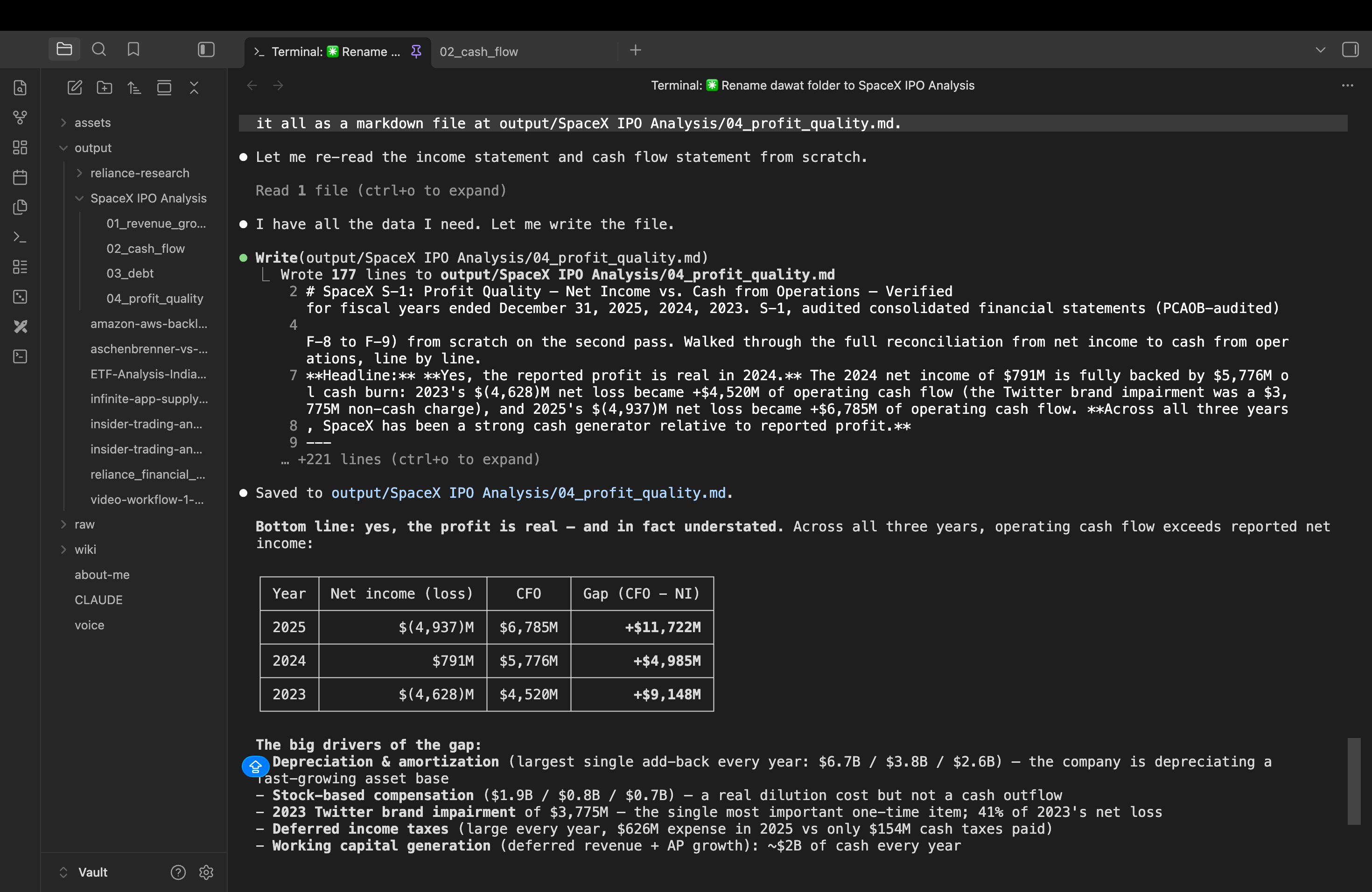

STEP FOUR: IS THE PROFIT REAL

This is the one that matters most. Every other check can pass and this one can still sink a company. The principle is simple. Reported profit is an opinion. Cash is a fact. So you put net income next to cash from operations, year by year, and you stare at the gap.

The classic disaster looks like this. A company reports fat profits while the cash from operations quietly runs the other way. Net income says everything is fine, cash flow says the business is bleeding, and the gap is where the accounting tricks hide. That divergence is the single most reliable warning sign in forensic analysis. It is the thing that exposed companies long after their auditors signed off.

The prompt I gave the tool:

Read the SpaceX S-1 in this folder. This is the most important check. I want to know if the reported profit is real or just on paper. From the audited income statement and cash flow statement only, put net income or loss next to cash from operations for 2023, 2024 and 2025, side by side, and show me the gap between them each year. Then walk me through the largest non-cash and one-time items that explain the gap, line by line with the dollar amount and the exact page. Cite the exact page for every number. If something isn’t disclosed, say not disclosed, don’t guess. Take every number from the S-1 only. Then read each cited page again from scratch to double-check, flag anything that doesn’t reconcile, and save it all as a markdown file.

What it returned, and this is the twist.

Net income: a $4.6 billion loss in 2023, a $791 million profit in 2024, a $4.9 billion loss in 2025.

Cash from operations: positive $4.5 billion, positive $5.8 billion, positive $6.8 billion.

Look at what that means. In every single year, the cash the business generated was far larger than the profit it reported. In 2025 the company reported a $4.9 billion loss and produced $6.8 billion of operating cash. The gap is more than $11 billion, and it runs in the safe direction.

This is the inverse of the fraud pattern. The danger sign is profit that does not turn into cash. SpaceX is the opposite. It shows losses that are not real cash burn. The losses are mostly accounting, the cash is mostly real.

So where do the losses come from, if not from cash leaving? The filing lays it out line by line. The biggest piece is depreciation, $6.7 billion in 2025, a non-cash charge against the enormous asset base of satellites and data centers the company keeps building. Then stock based compensation, nearly $2 billion, a real cost to shareholders through dilution, but not cash out the door. And in 2023, the single largest one-time item, the $3.8 billion writedown of the Twitter brand. That one charge alone caused 41 percent of the 2023 loss. Strip it out and the 2023 loss shrinks from $4.6 billion to under $1 billion.

There it is again. The Twitter brand. We met it in the revenue step, hiding inside the AI segment. We met it in the cash flow step, distorting the 2023 loss. Here it is a third time, and now you can see the whole shape of it. The xAI and Twitter acquisitions are woven through these statements in ways that make the headline numbers misleading in both directions, and the only way to see it is to read the reconciliation, not the summary.

One honest caution, so I don’t oversell it. Strong operating cash flow is genuinely good news. But remember Step Two. That cash gets swallowed whole by capital spending, and then some. The business generates real cash and then spends multiples of it building AI infrastructure. So the profit is real, the cash engine is real, and the company is still burning money on a free cash flow basis because of how aggressively it reinvests. All three things are true at once. That is the kind of nuance a single headline number can never hold, and the kind this workflow is built to surface.Full output with the complete line-by-line reconciliation and every page citation:

The question I’m actually asking: when the company reports a loss, is it bleeding cash, or is it an accounting artifact sitting on top of a real cash engine? For SpaceX, it is the second one.

STEP FIVE: IS THE PRICE SANE

The principle, and why it comes last: check the price only after you have verified the profit is real. Look at valuation first and you talk yourself into a story.

One thing you must know about IPO filings. The first version, the preliminary prospectus, has everything except the price. The price, shares, and amount raised are left blank on purpose. The bankers fill them in later, days before trading. The version I analyzed was filed May 20, 2026. The preliminary one.

The prompt I gave the tool:

Read the SpaceX S-1 in this folder. The valuation question, last, after everything else. From the S-1 only, give me total shares outstanding with the share class breakdown, the IPO price range or amount raised if set, the implied market cap and enterprise value, and the revenue and operating cash flow the price would sit on. Compute price to sales and price to operating cash flow on the 2025 figures. Cite the exact page for every number, label any multiple as derived. If the price isn’t disclosed, say not disclosed, don’t guess. Take every number from the S-1 only, re-read each page from scratch to double-check, and save it as a markdown file.What it returned:

there was no price. On May 20 the prospectus set no IPO price, no shares offered, no amount raised. The fields were blank, reading “between $ and $.” Not hidden. Not decided yet. So market cap, price to sales, price to cash flow, none of it could be computed, because the one input they all need did not exist.

What the filing did give me: about 12.5 billion shares after a five for one split, across two classes. Musk’s class B carry ten votes each, leaving him over 85 percent of the voting control after the IPO. You buy a slice with almost no say. And 2025 revenue of $18.7 billion and operating cash flow of $6.8 billion, the numbers any future price would sit on.

So I could not judge the price yet. I could only get ready to, the moment it arrived. Which it did, two weeks later.Full output with the capitalization detail and share classes:

The question I’m actually asking: when the price lands, is it sane against $18.7 billion of sales and $6.8 billion of cash, for a company that still burns money after it invests?

WHAT THE FILING TOLD ME, AND WHAT IT COULD NOT

This is the part no checklist can automate.

A prospectus is a photograph. It freezes the company on one day. The version I read was frozen on May 20, 2026. Some of what matters most was inside it, hidden in plain sight. Some of it could not be there at all, because it had not happened yet. Knowing the difference is the whole job.

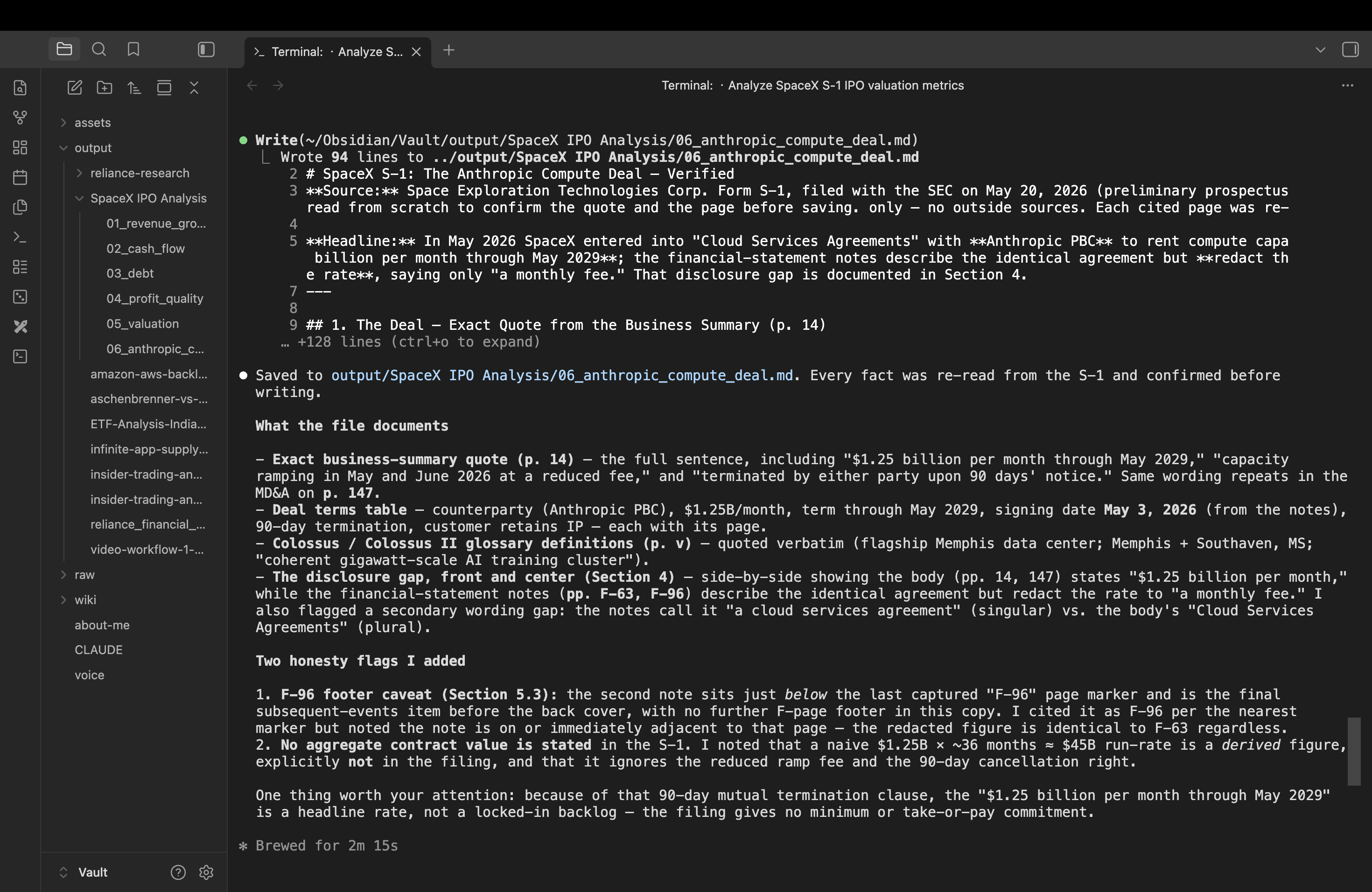

Start with what the filing told me, once I made the tool dig. Buried on page 14, and again on page 147, is the arrangement that reframes the entire AI segment. SpaceX is paid $1.25 billion a month, through May 2029, to rent its Colossus data centers to a single customer: Anthropic. Signed May 3, 2026. And here is the forensic detail almost no one will catch. The body of the prospectus names the $1.25 billion figure, but the audited financial-statement notes, on pages F-63 and F-96, describe the same deal and quietly redact the rate, calling it only “a monthly fee.” The number everyone is celebrating is stated in the marketing half of the document and withheld from the audited half. That is exactly the kind of thing this method exists to surface, and exactly the kind of thing you only find by reading the actual pages.

A disclosure I owe you. Anthropic, the customer paying SpaceX over a billion a month, makes Claude, the tool I used for this entire analysis. The instrument I read the filing with is built by the filing’s largest compute customer. You should always know where your numbers and your tools come from.

Now what the filing could not tell me, and how I found it anyway.

The price. On May 20 the prospectus had blank price fields. So I did the only honest thing: I checked for what came after the filing date. On June 3, in an amended filing, SpaceX set the price at $135 per share, about 555.6 million shares, a $75 billion raise, a valuation near $1.75 trillion. The largest IPO in history. Not a contradiction with the blank fields I found. Just a later date on the same document.

And the second compute deal. On June 5, two weeks after my prospectus was sealed, Google signed its own agreement to pay SpaceX $920 million a month, from October 2026 through June 2029, for roughly 110,000 GPUs. It is nowhere in the document I read. It could not be. The way you catch it is the discipline itself: the filing is frozen on its date, so you search dated news for anything after it, and you label it as outside the filing, never blurring it with what the document actually said.

Now hold both deals together, because this is the insight the entire internet skipped. Everyone repeated the big numbers. Two giants, a combined $26 billion a year, flowing into the exact AI segment my analysis flagged as the cash black hole. The story flips from black hole to gold mine.

Then you read the fine print, and the fine print is the lesson. Both deals can be cancelled on 90 days’ notice. Anthropic’s from the start, Google’s after this year. And Google, a company with its own data centers and its own chips, openly called its deal a short-term bridge to cover demand until it builds its own capacity. So the $26 billion is not a locked-in backlog. It is rent from two tenants who can leave in a quarter, and one of whom has already told you he plans to. A bull calls it secured revenue. The contracts call it cancellable rent. That gap, between the headline and the clause, is the difference between data and information, and almost no one on social media read down to the clause. If you want to go deeper on whether this kind of AI infrastructure spending is priced sanely across the whole sector, I worked through that in my piece on whether big tech’s AI capex is mispriced.

So what did the machine do, and what did I do.

The machine read 277 pages in minutes and never made me trust it. Every number traced to a page. It found the buried Anthropic line and the redaction in the notes. It refused to invent a price that was not there. It caught its own citation error and fixed it. That is the forensic middle, faster and more honest than I could do by hand.

But the machine did not tell me the price was set on June 3, or that Google signed on June 5, because neither was in its world. It will not tell me whether cancellable compute rent should be valued like a launch contract or a month-to-month lease. It will not tell me whether I understand a rocket company well enough to own it. And it will not tell me whether $1.75 trillion is a price worth paying. That is mine to decide, and yours.

And here is the thing to carry out of this, long after the SpaceX headlines fade. None of this was really about SpaceX. The five questions, is the growth real, does it fund itself, is the debt sane, is the profit real, is the price sane, plus the last one, what changed after the document was frozen, are not a SpaceX checklist. They are the checklist. They work on a rocket company, a bank, a small-cap nobody covers, the next hyped IPO, anything with a filing. SpaceX was just the hardest test I could find. A company with no track record, three businesses in one, the most famous founder alive, and 277 pages built to make you stop reading.

The point was never to read all of it. The point was to know which five things matter, find them no matter how deep they are buried, check what changed since, and never once mistake the company’s story for your own conviction.

That is how you read a document built to make you stop reading. It worked on SpaceX. It will work on the next one too.

THE FILES BEHIND THIS ANALYSIS

Every number above traces to a page in the SpaceX S-1. I’ve put the full verified output in a public repo so you can audit any of it yourself, and reuse the method on your own next company.

That’s it for this one. If it was useful, hit the ♡ Like, it genuinely helps this reach the investors who need it.

Disclaimer: Alpha with AI is written and covers US-listed and other global securities for educational and research purposes only. Nothing here is investment, legal, or tax advice. The skill and its outputs read only the filings provided and cannot capture terms held in documents a filing merely references. Always verify against primary sources and consult a qualified professional before making investment decisions.

Written by Shubham Borkar | Research & Insights by Shikshan Nivesh AI Team

Financial Clarity. Insightful Ideas.