Research Dive #1: Accenture (ACN)

Why is Accenture (ACN) down 55%? The bear case is in its own 10-K, the AI metric is missing from its earnings releases, and the valuation is my math, shown.

In February I wrote that the traditional IT middleman was dead.

I meant it. That edition argued AI was collapsing the cost of building software to almost nothing, and that the people who bill by the hour to build it for you were standing exactly where the flood would hit first. Within a week the market agreed, loudly, and billable-hour businesses everywhere repriced. (If you missed it, the argument lives here: the traditional IT middleman is dead.)

Then, on the 22nd of June, I placed a buy order for the biggest billable-hours firm on the planet.

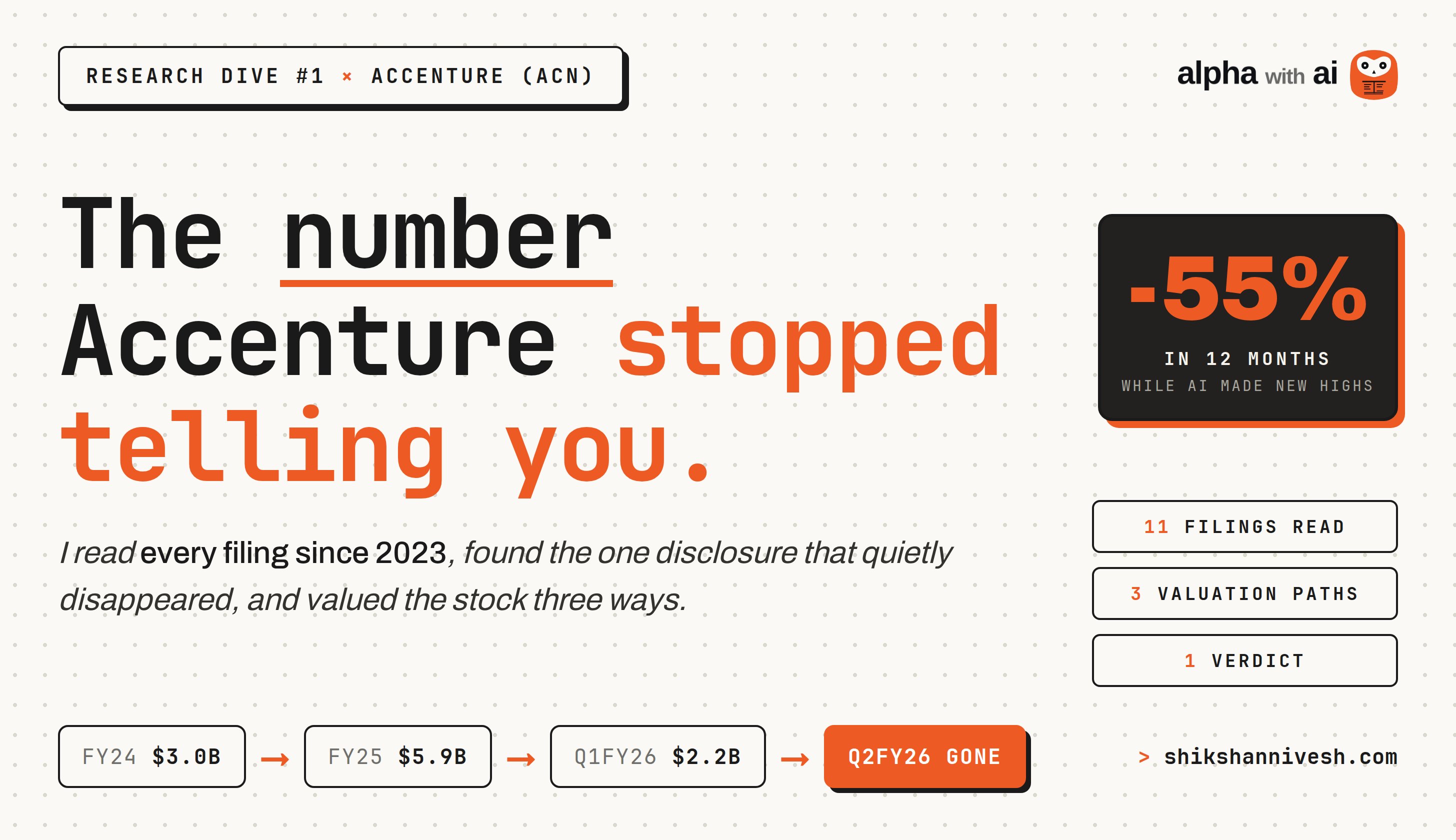

Accenture. Nearly eight hundred thousand people. The firm that boards call when they want change made without their own fingerprints on it. The stock had been cut in half in twelve months while everything else with AI in the story made new highs, and somewhere in that gap I stopped seeing an AI casualty and started seeing a mispricing.

Now, I usually never buy a position in one go. I accumulate. Small orders, spaced out, so the market has time to prove me wrong before I am fully in. What I placed that morning was the first of those small orders. A toe in the water, nothing more.

Here is the confession this edition is built on.

While preparing this deep dive, I opened my account to check my cost basis. There was no cost basis to check. The order never went through, and I had spent two weeks believing my accumulation had started when it had not. The stock is up around ten percent since. That stings more than a loss would. A loss at least means you acted.

So I am not writing this to defend a position. I do not have one. I am writing it to decide, with the filings open and you watching, whether that first order deserves to be placed again. And I do not get to shrug my way to an answer. Both of my bets are already on the table. I wrote the bear case in February. I placed the bull order in June. One of those two people was wrong, and this edition finds out which one.

Before we open a single filing, you should know something about this company. The market has sentenced Accenture to death twice before.

The first sentence came from its own family. Accenture began as the consulting arm of Arthur Andersen, the accounting giant, and by the late nineties the consultants were the ones making the money, handing up to fifteen percent of their profits to the parent nearly every year. They wanted out. The divorce took years of arbitration, and in August 2000 the ruling came down. The parent had demanded roughly fourteen and a half billion dollars. The arbitrator awarded it no damages at all. Just the roughly one billion dollars of profit-sharing money it was owed anyway, half of it already sitting in escrow, and one condition: surrender the Andersen name entirely, and go. An employee in the firm’s Oslo office named Kim Petersen won the internal naming contest with a made-up word, accent on the future, and in January 2001 Andersen Consulting became Accenture.

Within a year, the name it had been forced to surrender was radioactive. Arthur Andersen was Enron’s auditor, and it did not survive the scandal. Almost a century of reputation, gone. The orphan that paid a billion dollars to lose its family name had bought, by pure accident, the cheapest insurance in corporate history. It listed at $14.50 a share in July 2001 and spent the next two decades compounding into the largest technology consultancy on earth.

The second death sentence came a decade ago, and it will sound familiar. Cloud software was going to make integrators obsolete. Why pay consultants by the hour when the solution arrives turn-key, out of the box? You know how that ended. In the decade that followed, revenue more than doubled.

Now the third sentence has been handed down, and this time the executioner is supposed to be AI. AI writes the code, drafts the deck, does the work. Who needs eight hundred thousand consultants? The market believes AI is the largest business transformation of our lifetime, and it also believes the firm hired to run that transformation is dying of it. Both of those cannot be fully true at the same time.

Maybe the third sentence is the one that sticks. Companies do not get infinite lives, and sometimes the scare everyone laughed off twice is real the third time. That is exactly what this deep dive exists to find out.

I pointed Claude Code at every annual report, quarterly filing and earnings release Accenture has put on EDGAR since 2023. Eleven documents, every number pulled straight from the source, and one standing instruction: build the case against me.

(The whole rig, Claude Code running inside Obsidian with every filing it pulls saved into the vault, is its own edition: how I set up Claude Code as my investment research analyst, and the 2.0 rebuild that moved everything inside Obsidian. Start there if you want to run this yourself.)

What came back is stranger than the bull story or the bear story. There is a number Accenture spent two fiscal years leading its earnings releases with, and this year it quietly stopped appearing.

Hold that. We will get to it.

Quick context before we go in. I build the AI research workflows I wish I’d had on the equity desk, then show you exactly how they run on real companies. Free to join ~5000 investors reading along. Subscribe and the next one lands in your inbox.

THE 60-SECOND THESIS

What they do. The world’s largest technology consultancy. 799,000 people, split almost exactly in half between designing large corporate transformations (consulting) and running the systems those transformations produce (managed services), on $69.7 billion of FY2025 revenue. Almost none of it needs capital: $600 million of capex against $10.9 billion of free cash flow last year. The asset is people billed by the hour. Which is exactly what the market has turned against.

Why it is down. The market has repriced Accenture as an AI casualty, and the dents are real, not imagined. Local-currency growth slowed 5, then 4, then 3 percent through FY2026. The US federal business, 8 percent of revenue, is being cut under DOGE (the US government cost-cutting department) and costs about a point of growth. Managed services bookings (new contracts signed, the order book), the bigger half of the business, fell 16 percent last quarter. Even the filing language has cooled: pricing went from “improved in several areas” to “relatively stable”.

Why I think that is the mispricing. Cut in half in a year, Accenture now trades at a free cash flow yield near 13 percent on management’s own $10.8 to 11.5 billion guide, by my math. The company is priced for decay and guiding for growth. One of those two is wrong. My view, and the reason for that June order: in the near term, everyone wants AI and almost nobody can implement it. Accenture has logged 104 quarterly client bookings of $100 million or more so far this year, up 13 percent, and its filings say clients keep prioritizing large-scale transformations to become AI-ready. Structurally, I believe companies hire Accenture for reasons AI does not remove: cover for hard decisions, someone else to blame, and speed they do not have in-house. That is an opinion, not a fact. The rest of this piece exists to test it.

What could turn it. The federal drag stops being news, since the guide already implies 4 to 5 percent growth without it. Capital returns the price ignores: a buyback raised to $7.5 billion, a dividend up 10 percent, $5 billion of net cash still on the books. And AI bookings visibly converting into revenue. Whether AI replaces the billable hour faster than it deflates it is the question that decides everything, and there is one number, quietly missing from the last two earnings releases, that sits at the center of it. Both get their full sections below.

THE BUSINESS IN ONE LENS

Most coverage treats Accenture as one giant consulting firm. The filings describe something more interesting: two different businesses wearing one badge, and AI is hitting them in opposite ways.

The first business is consulting. Senior people who design large transformations, project by project. That was $35.1 billion of revenue last year, growing 5 percent in local currency. The second business is managed services: multi-year contracts to run the systems and operations those transformations leave behind. That was $34.6 billion, growing 9 percent. And in the first nine months of this fiscal year, the second business became the bigger one for the first time, $27.9 billion against $27.6 billion. I had Claude Code pull the revenue tables from the last three 10-Qs and reconcile the two halves quarter by quarter, and that crossover is the quietest important fact in the filings.

Why it matters: consulting is where an AI wave shows up first as demand. Someone has to design the transformation, pick the models, rewire the workflows. Managed services is where AI shows up as deflation. It is the running of systems, the processing of invoices and claims and tickets, the recurring human hours that agents are supposed to replace. Same company, opposite exposure. You are not buying one bet on AI. You are buying both sides of it, in one stock.

And in the latest quarter, the two halves diverged exactly along that line. Consulting bookings rose 11 percent in local currency. Managed services bookings fell 16. One honest caveat before anyone extrapolates a single quarter: bookings are lumpy, and a handful of mega-deals moving by a few weeks can swing that number. But the direction matches the exact fear the market is pricing, and it is the line I will be watching hardest from here.

Step back and the machine itself looks nothing like a company in decline.

Margins tell the honest version: operating margin was 14.7 percent last year on a GAAP basis, 15.6 adjusted, and gross margin actually slipped to 31.9 percent, which the 10-K attributes to higher payroll costs. This is not a business getting more profitable per hour. It is a business getting bigger while paying more for its people. Hold that tension; it comes back in the hinge.

Geographically, the Americas are half the company, EMEA about a third, and Asia Pacific, the smallest slice, is suddenly the fastest growing at 9 percent. The balance sheet fits in one line: $10.2 billion of cash against $5.1 billion of debt, the first term debt in the company’s history, which is its own story for later. (Reading what sits above the equity holder is a discipline with its own edition: the whole debt structure from one filing.)

This is the machine the Andersen orphan built: capital-light, cash-gushing, buying a handful of small firms every year as its R&D department, and handing everything left over back to shareholders. The question this piece exists to answer is not whether the machine works. It is whether AI changes what the machine gets paid for.

WHY IT’S DOWN

The company admits the bear case in writing

I did not find the strongest version of the bear case in a short report or on a podcast. I found it in Accenture’s own annual report. I had Claude Code read the FY2025 10-K’s risk factors and pull every sentence about AI, and this one deserves to be read slowly:

“Some services and tasks currently performed by our people have been and will continue to be replaced by automation, including AI-enabled solutions, which will lead to reduced demand for our services and/or adversely affect the utilisation rate of our professionals, if demand for those services is not replaced by demand for new solutions and services... If we are unable to introduce or if our clients do not accept new pricing or commercial models that reflect the value of these AI-enabled solutions, our results of operations may be adversely affected.”

Not “may be replaced.” Will, unless new demand replaces what automation takes. The company that sells the AI transition has told its own shareholders, in a filed document, that AI shrinks the thing it currently bills for, and that survival means selling something new in its place. The whole stock is a bet on that unless. Everything else in this section is that sentence showing up in the numbers.

The growth is slower than the headline

Reported revenue grew 6, 8, and 6 percent across the three quarters of FY2026. Strip out currency and it is 5, then 4, then 3. The dollar did the flattering: foreign exchange added as much as 4.4 points in a single quarter. Management’s own full-year guide has narrowed from 2 to 5 percent in local currency to 3 to 4, with the top end doing the falling.

Washington took a bite

Accenture Federal Services was 8 percent of revenue last year, and roughly a third of the Health and Public Service group. Under DOGE, the filings describe procurement delays, price reductions, contract scope cuts, and outright terminations, with the GSA instructing every federal agency to review its consulting contracts. The result: a segment that grew 6 percent last year is shrinking this year, and management pegs the drag at about one point of total company growth, roughly $700 million by my math. There is also an open Department of Justice matter at the federal unit; it belongs in the risk section, and I will come back to it there.

The order book cooled exactly where it hurts

Full-year bookings actually fell 1 percent in FY2025. This year started strong, then Q3 brought the number that matters: total bookings down 3 percent in local currency, and managed services bookings, the bigger half of the business, down 16. And the filings’ language about pricing has been quietly walking backwards. I had Claude Code line up the same sentence in the MD&A (the management commentary section of a filing) across four consecutive filings: “improved in several areas” became “improved in some areas” became “relatively stable.” That is how pricing pressure sounds when a company is choosing its words carefully.

The margin is being defended, not expanding

Gross margin fell 70 basis points last year to 31.9 percent, the payroll squeeze from the last section. The operating margin held up, but look at how: a $923 million severance and “business optimization” program that cut roughly 22,000 people from the February 2025 peak, though hiring has since resumed, and utilization (the share of employee time billed to clients) pushed to 93 percent, the highest level anywhere in these filings. The 10-K itself warns that utilization run too high damages engagement and drives attrition. Squeezing harder is a strategy with a ceiling.

And the challengers are smaller, faster, and sometimes your own client

The 10-K names the competition plainly: clients and ecosystem partners building their own AI capability, and “new AI-native companies.” The structural fear is simple. If AI collapses the cost of delivering technology work, the advantage of an 800,000-person pyramid built on billable hours inverts. Every mid-size AI-native shop is pitching exactly that story to Accenture’s clients right now.

Add it up and this is not a stock that fell on a misunderstanding. The bear case is coherent, filed, and partly visible in the numbers already. The market looked at all of it and cut the price in half.

The only question that matters is whether it stopped at the right floor. That question has one hinge, and the company’s own disclosures, including one number that quietly disappeared, are where we go next.

This is where the paid section begins. The free half gave you the setup, the history, and the honest bear case. The paid half takes the hinge apart, shows the number that vanished, and lands on what I am doing with that June order.